1. Why Stablecoins Matter

Stablecoins are the silent backbone of crypto. They’re the bridge between TradFi and DeFi, powering everything from DEX liquidity to cross-border payments and on-chain treasuries.

With over $160B in total stablecoins issued, they rival the GDP of small countries.

Now, even Big Tech is circling.

Adoption is accelerating beyond crypto. Apple, Google, Airbnb, and X are exploring stablecoins for payments and rewards, signaling a shift: stablecoins are becoming part of global financial infrastructure.

2. Circle in Focus

Circle is the issuer of USDC, the second-largest stablecoin by market cap. But it’s not just a token issuer. Circle is building regulated digital dollar rails — and it’s now publicly traded on the NYSE under ticker CRCL.

Circle debuted with a $31 share price, skyrocketed to $83.23 on day one, and currently trades at $115.25, implying a ~$28B market cap.

💡 Good News for Sigil Core Investors

Sigil Core invested in Circle in July 2024, well before its public debut. On IPO day alone, this position delivered a +9% gain to the fund’s NAV — and the total return has now reached ~4x within a year.

Buying future winners in advance is one of the key ways Sigil Core generates alpha for its investors.

3. Investment Thesis

We’re bullish on stablecoins — and Circle is the only clean investable way to express that thesis on the stockmarket.

- IPO catalyst realized: Now liquid and tradable

- Regulatory edge: Circle is U.S.-regulated, unlike Tether

- Growing market: Stablecoins are eating cross-border payments

- Public market entry: ~$28B valuation with potential upside

- Anticipated regulatory tailwinds post-2024 U.S. elections, with expectations of a more favorable policy environment for crypto-native companies like Circle.

Circle is not a market leader, but it is the only investable stablecoin infra play.

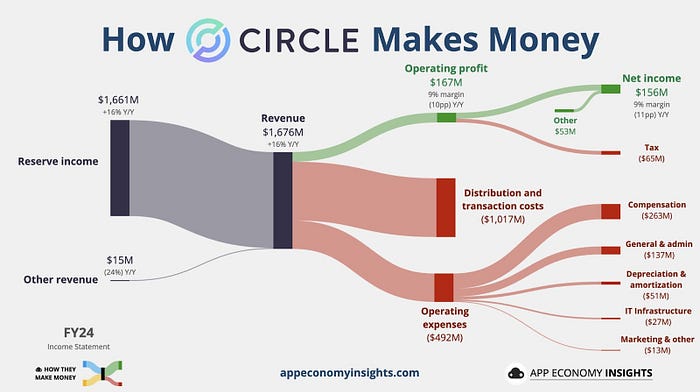

4. Revenue Breakdown

Circle earns revenue primarily through interest on reserve assets — real U.S. dollars held in custodial banks or short-term government debt.

To explain simply:

- For every 1 USDC issued, Circle holds 1 real U.S. dollar

- These dollars are stored in short-term Treasuries and repo agreements

- While held, they generate yield — driven by Federal Reserve interest rates

This forms the backbone of Circle’s business model.

Reserve Snapshot:

- ~$33B in reserves

- $11B in U.S. Treasuries (short-term)

- $16B in repo agreements (5.3%–5.4% APR)

Circle effectively lends the reserves backing USDC to the U.S. government and large institutions, earning interest in return.

- Annualized gross yield: ~$1.46B

- Net of Coinbase revenue share (~$800M/year), Circle clears at least $650–700M/year.

Circle currently charges no fees on minting/redeeming USDC — improving peg stability, but potentially reducing revenue when Fed rates decline.

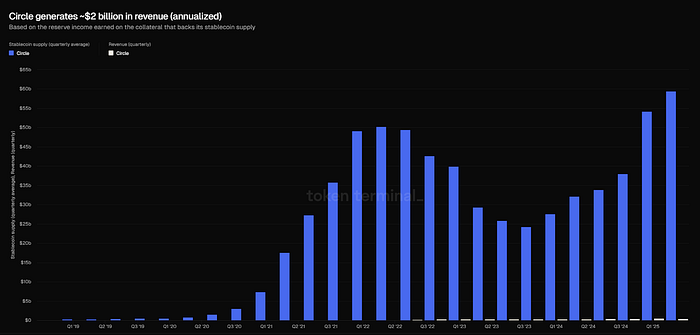

5. Financials

https://tokenterminal.com/explorer/studio/dashboards/98e3128c-502d-42da-8396-b7539ece9581?

FY 2024 revenue: $1.68B

FY 2024 net income: $157M

Q1 2025 revenue: $578.6M

Q1 2025 net income: $64.8M

Trailing 12 months (to Mar 2025):

Total revenue: $1.89B

Gross profit: $453M

Operating income: $207.8M

Net income: $173M

Balance Sheet Highlights:

Cash & short-term investments: ~$61.3B

Net cash per share: ~$830

Debt: Minimal (~$53M)

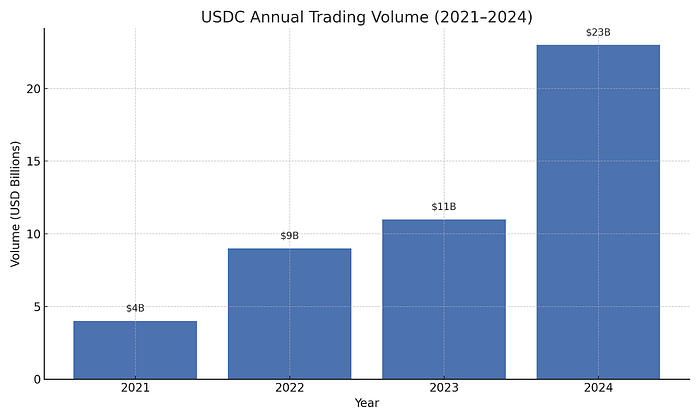

6. USDC Volume Trends

- USDC recorded $23B trading volume in 2024 — more than double compared to 2023.

- Exchange-centric activity now represents ~90% of total USDC volumes, driven by institutional and pro-trader use.

Takeaways:

- Strong liquidity pump — Daily trading in multibillions supports active use across exchanges and DeFi platforms.

- High transfer throughput — On-chain flows indicate institutional and retail demand beyond simple trading.

- Maintained peg and trust — Large, consistent volumes reflect sustained confidence post-peg event.

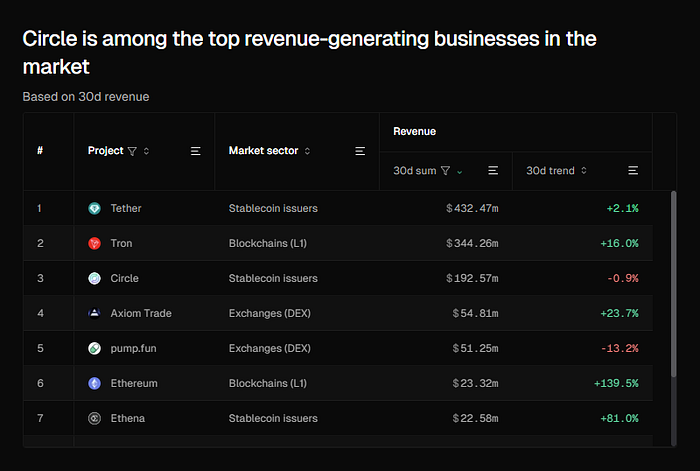

7. The Competition

Tether dominates in Asia and emerging markets, but Circle holds the edge in:

- Regulatory clarity

- Institutional trust

- Western financial integrations

If stablecoins win in the U.S. and Europe, Circle wins.

https://tokenterminal.com/explorer/studio/dashboards/98e3128c-502d-42da-8396-b7539ece9581?

8. Catalysts

- Rising regulatory pressure on Tether

- Big Tech adoption of stablecoins

- U.S. anti-CBDC sentiment boosts private stablecoins

9. Risks & Thesis Invalidation

1. Margin Compression from Distribution Costs

Circle’s core revenue — interest on USDC reserves — is eroded by significant payouts to distribution partners, especially Coinbase. In 2024, over 60% of revenue was shared, with Coinbase alone accounting for ~$800M annually. This structural revenue-sharing model limits Circle’s ability to expand margins despite strong top-line growth.

2. Sensitivity to U.S. Interest Rates

The majority of Circle’s income comes from yield on short-term Treasuries and repo markets. A decline in Fed rates would directly reduce gross revenue. While Circle argues that lower rates stimulate stablecoin usage, the offsetting fee-based services business remains nascent.

3. Increasing Competitive Pressure

The stablecoin landscape is becoming increasingly saturated. Tether continues to dominate ($154B supply), while Paxos, fintechs, and banks — including those developing proprietary stablecoins — threaten Circle’s distribution.

4. Regulatory Risk Shifts

While U.S. legislation may favor Circle, international frameworks remain uncertain and could limit global expansion.

Thesis Invalidation Triggers:

- Significant Fed rate cuts without equivalent growth in fee revenue

- USDC fails to achieve adoption beyond exchanges

- Disruption by new entrants (banks, Big Tech, sovereign-backed stablecoins)

- Regulatory momentum shifts away from Circle’s model

10. Final Take

Circle is no longer a speculative crypto play. It’s a publicly traded, revenue-generating infrastructure layer for digital dollars.

In a world where Big Tech and TradFi converge with blockchain rails, Circle sits at the intersection of it all.

It’s regulated. It’s cash-rich. It’s profitable.

And now, it’s investable.

Sigil invested at a $5B FDV valuation pre-IPO.

Disclaimer: This is not financial advice. Always do your own research before making investment decisions.