Key Highlights:

- Trump Effect: Deregulation hype turned to chaos via memecoins and geopolitics.

- Sigil Core: Experienced drawdown amid systemic shocks; capital redeployed into high-conviction positions.

- Sigil Stable: Delivered +5.39% net yield despite broad market decline, reinforcing its role as a stable, uncorrelated return source.

- Outlook: Elevated volatility expected, but crypto poised for tailwinds in the long run.

Dear Investors,

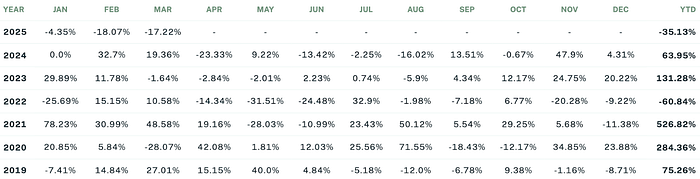

In the Q1 of 2025, Sigil Core recorded -35.12% vs EUR, -32.18% vs USD, -23.14% vs BTC. Total crypto market capitalization fell by 18.6% — from $3.39 trillion to $2.76 trillion.

Sigil Core Net Performance vs EUR Q1 2025

Navigating Geopolitical Shockwaves

This letter will be a bit different from what you may be used to. We will be talking a bit more about topics outside of cool tech crypto innovation. But please indulge me, because events from the last 3 months are asking for proper coverage. Also I apologise upfront if some of my commentaries challenge your political opinions. In general, I am largely apolitical but when politics affects the markets too much, I am compelled to form a view in an attempt to navigate them better.

Q1 2025 was probably the hardest period in my investing career. It wasn’t the hardest to navigate because crypto went down or because we saw some turbulent macro events — these things had happened before. It was the hardest to navigate because never before have we seen such a big mismatch between market expectation and reality. Never before have we seen such a direct and immediate impact of one politician (albeit the most powerful one) not only on crypto but on the very fabric of our current economic world order.

Since Sigil’s inception in 2018, we shied away from using macro and geopolitical events for our decision making. I have always maintained the position that those were unpredictable, and even if some select few could generate an edge trading them, it was certainly not me or our team.

We have always been crypto tech investors, betting on disruptive tech that will topple the market incumbents. This is the first time I feel the need to form a guiding opinion on the state of the geopolitical landscape, while being fully aware that these days any macro and political predictions are prone to be wrong even more than usual.

The Trump Effect

When Donald Trump got elected, it sparked a wave of optimism in both traditional markets and in crypto. The crypto industry specifically had a reason to celebrate. After 4 years of “Operation Chokepoint” when the US administration and the SEC put pressure on crypto through regulation via enforcement and restricting access to banking. Trump, while slightly anti-crypto in his first term, took over crypto by storm during his second campaign. He led with promises of deregulation and even putting crypto and blockchain tech at the centre of the US national interest. While I expected many of Trump’s promises to be populist tactics, I still welcomed the de-regulation rhetoric. In my opinion, our industry doesn’t need that much from the US government. Crypto builders just need the SEC to get off their backs for a while and let them cook.

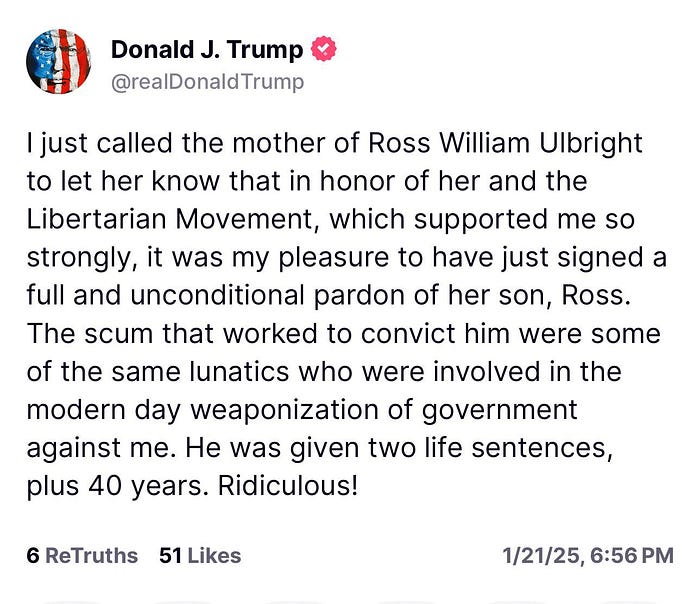

Ross Ulbricht was a founder of Silk Road — dark web marketplace operating mostly with Bitcoin payments. After his extreme sentence he was viewed by the ideological crypto community as a martyr. Trump pardon was a very positive signal for crypto and its ideals.

Trump, however, didn’t stop at simply getting out of our way. Even before he took office, he became an active and influential agent within our ecosystem. Apart from his NFT collectibles, his team launched World Liberty Finance — a DeFi protocol on Ethereum which had a mixed reception. The final straw, however, came with the launch of TRUMP memecoin on Solana, mere days before inauguration, which was quickly followed by the MELANIA memecoin. Insiders around Trump extracted hundreds of millions of USD from these coins over the first few days.

TRUMP memecoin price went all the way to 73 USD, putting its market cap at over 8 billion dollars and fully diluted valuation (counting with majority of tokens which remained locked) at 73 billion USD.

MELANIA saw moderate success, shooting quickly to 14 USD (14 billion USD fully diluted valuation). Both tokens captured huge interest of speculators and commentators alike, however after their initial pump, they met the fate of most memecoins.

In retrospect these events marked the market top. What followed was a series of dodgy launches, among them the token endorsed by Argentinian president Javier Milei with an even worse outcome for speculators. This was met with mixed reactions and it looked like Trump’s crypto shenanigans signal to the market that anything goes now and builders (and unfortunately also scammers) have a free hand to experiment.

However, these crypto events quickly became overshadowed by Trump’s dubious actions in the geopolitical and economic arena. In the first 2 months of Trump’s presidency he managed to put American ties with closest allies into jeopardy by adopting various aggressive postures and aligning with unfriendly countries, threatening to annex Canada and Greenland, while abandoning Ukrainian cause to squarely side with Putin’s talking points on the matter.

While these actions certainly started a spark of uncertainty across the global risk-on markets, the final nail in the optimist’s coffin was undoubtedly the severe economic tariff policy and the chaotic way it was communicated, seemingly flip-flopping between hawkish and dovish positions. I could keep going on, but this is the reality we live in now and possibly for the next 3 years. We can only hope the threatening phase is over and we will finally see some beautiful “Art of The Deal” phase.

Positioning and Portfolio Updates

Directional predictions about the market and macroeconomic forecasts are difficult in any set of conditions, but now they are even more likely to fail. That being said, I wouldn’t be surprised to see the American pole position in capital markets being somewhat challenged, as some investors will try to diversify out of USD and US markets elsewhere. At the same time, it is hard to expect capital allocators to find many satisfying alternatives to the US markets. The USA is still the dominant economic and robust geopolitical power and we will probably not see it being completely undone during one chaotic presidential term.

My base case for the general market sentiment during Trump’s term is that we will be facing elevated headline risk, uncertainty and volatility, together with multi-faceted secular tailwinds for crypto:

- Crypto as an asset class and crypto businesses are largely not directly affected by tariffs, with the exception of hardware based businesses such as PoW mining. Some verticals may even play a role in bypassing them and providing alternative means of payments to the grey economy that will likely form around market inefficiencies created by tariffs.

- The SEC is taking a backseat and we are seeing ongoing positive (albeit chaotic) rhetoric about crypto from the Trump admin. We are seeing a lot of big tech companies and traditional financial institutions taking unprecedented interest in crypto, not just as an investment asset but also as a technology to build on, to expand and improve their own business.

- Increased market uncertainty may lead many capital allocators to diversify outside of the US markets. Some of them will view crypto as an appealing, tariff-resistant alternative for their portfolio diversification.

- Tariffs and economic war with China may cause a global recession, forcing the Fed to end the 4 year era of monetary tightening and start stimulating. This was always bullish for risk-on assets in general and crypto in particular. Interestingly, the positive outcome of US-China deal making could be bullish for crypto too, if part of the deal is weaker USD policy allowing China to fully unleash the money printer.

Given all of the above, we remain structurally bullish and positioned long, although we expect more of a volatile and uncertain ride rather than a smooth bull cycle.

It is my job as a CIO to also look at the potential counter-signals to our positioning. Apart from macroeconomic changes that are very hard to forecast and act upon in time, things that would force me to reconsider our bullish bias are mostly in the realm of disruptive geopolitical tail risks.

The famous ChatGPT formula is on display, with POTUS proudly putting tariffs on penguin inhabited islands.

The US and China are basically in a cold war which now entered a new more explicit stage with Trump’s tariffs. Other recent events already showed us that kinetic wars between big powers are not off the table either. The end of the Russo-Ukrainian war seems to be far away, Israel is struggling with Iran and its proxies, China continues tightening its noose around Taiwan and India and Pakistan have renewed their border dispute in Kashmir.

Any of these conflicts has a potential to escalate and involve more powers, which would be undeniably bearish for tech optimistic risk. On the other hand any significant de-escalation and signs of “getting back to normal” will undoubtedly inspire more optimism. Amidst all the chaos it’s good to remember that most of us simply want to live in peace and improve the quality of life for ourselves and our close ones. Science, technology and free trade are three single biggest contributors to the prosperity and growth of humanity in general.

All of the above is high level commentary for the next 3 years. When we zoom in for the next quarter, we expect markets to stabilize as they are absorbing the shock from the unexpected tariff policies. The big day to watch out for will be July 8th when the 3 month tariff freeze for all countries (except China) ends. Unless we get some unexpected resolution beforehand, we will likely enter another round of tariff-related chaos.

If you’re coming to our letters with a view to learn more about our strategies and portfolio, I apologise for a longer than usual detour into the world of politics. Let me at least give you a few points:

Bitcoin

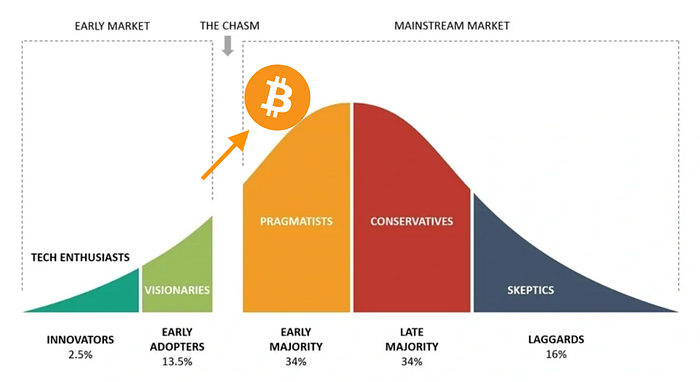

We can safely proclaim that Bitcoin managed to cross the chasm from early innovation and niche assets into the mainstream. It takes the world of traditional finance by storm with record breaking ETF flows, a bit of financial engineering from Microstrategy and an easy to understand narrative as “digital gold”. That certainly helps in a world where gold breaks all time highs. We are seeing institutions, corporations and even state actors considering strategic bitcoin reserves. This sort of liquidity is very different from the average retail speculator. The train starts moving slowly but when it picks up speed it becomes unstoppable. Hence BTC remains our largest position to capitalise on this potential long term secular trend.

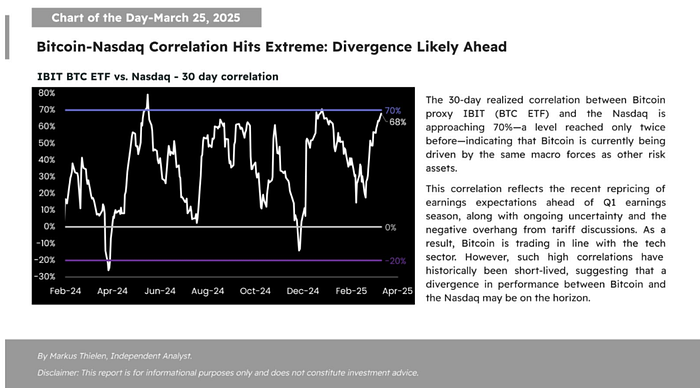

You may also ask “Isn’t Bitcoin supposed to be an anti-systemic hedge against uncertainty?” Well, sort of. Bitcoin currently still trades like “80% NASDAQ, 20% Gold” but more and more investors start to consider it as an alternative asset to gold and act as a possible escape hatch for capital in crisis situations. This may become a self fulfilling prophecy, making Bitcoin less correlated to tech equities.

Robinhood

We are also observing a fast accelerating trend of successful traditional companies adopting crypto. One such company is Robinhood — one of the most popular trading and investing retail apps. Throughout Q4 2024 crypto was their fastest growing segment by volume traded. On top of that they are actively looking to build new features directly on crypto rails and integrate parts of their business on-chain. Sigil Core holds a position in Robinhood (HOOD), which brings a bit of a traditional stock exposure into our portfolio dominated by digital assets.

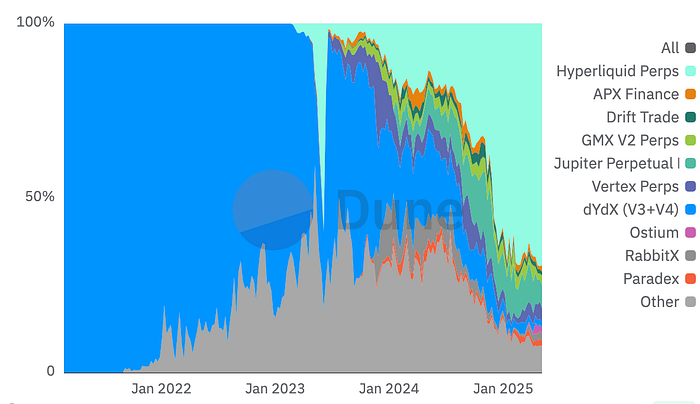

Hyperliquid

One of our highest conviction positions is Hyperliquid (HYPE). The project keeps growing across all relevant metrics and establishing itself as a category winner. It’s winning not only in the decentralised perpetual futures market but it starts to rival centralised exchanges as well. On top of that it becomes a standalone DeFi ecosystem with other DeFi projects building on top of it. We will cover Hyperliquid in detail in a standalone research article.

Hyperliquid dominated the market share of decentralised perp platforms. We think it is time to challenge its centralized counterparts as well.

Recent rebalance

In January 2025 we decreased our long exposure from 100% to 80%. Now our long exposure is around 90%, taking advantage of discount prices and reflecting our largely bullish view even in the face of uncertainty.

I would like to note that our investors are advised to hold a combined portfolio of Sigil Core and Sigil Stable with weights reflecting their own individual risk appetite. Sigil Core by itself is a risk-on high volatility vehicle which requires nerves of steel to ride. Sigil Stable can balance your volatile Core exposure with more… stability.

Sigil Stable

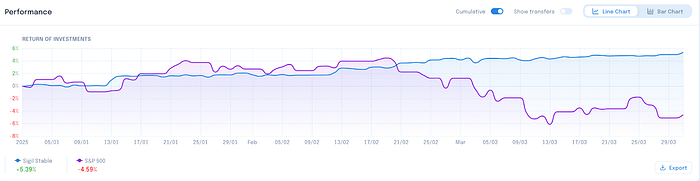

Despite an 18.6% decline in the total crypto market capitalization — from $3.39 trillion to $2.76 trillion during Q1 — Sigil Stable delivered a solid 5.39% net yield after fees for our investors.

Sigil Stable Net Performance vs USD Q1 2025

With a Sharpe ratio of 3.99, the fund continues to fulfill its core mandate: providing safety, stability, and low correlation in diversified portfolios. For comparison, the S&P 500 returned -4.59% over the same period.

Strategy Update: Agility in a Shifting Market

Sigil Stable continues to pursue a multi-strategy, market-neutral approach, designed to adapt dynamically to evolving market conditions in pursuit of the most attractive risk-adjusted returns.

Basis Trades and Tactical Rebalancing

Our allocation to basis trades peaked at over 30% in January, capitalizing on dislocations during the launch of high-profile meme coins like $TRUMP, $HYPE, $FARTCOIN, and $PENGU. These trades performed exceptionally well during a highly active period.

However, as the broader market turned bearish, basis trade opportunities became significantly less attractive in February and March. In response, we sharply reduced our exposure and redeployed capital into more compelling yield-generating strategies demonstrating the fund’s ability to pivot.

Private Yield Deals

In February, we concluded a private liquidity agreement with a crypto foundation that had been active for a full year and delivered an annualized yield exceeding 30%. In March, we renewed a liquidity provisioning partnership with a DAO-backed project, where we also hold a discretionary long position via the Core fund. That same month, we entered into a new private deal with an undisclosed counterparty. While confidentiality clauses prevent further detail, we remain focused on sourcing asymmetric yield opportunities from non-public channels.

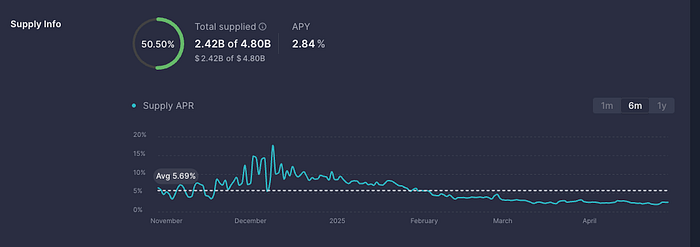

Public Yield Farming & Stablecoin Deployment

Stablecoin yields in public money markets compressed sharply in Q1. The chart below illustrates declining USDC lending rates on Aave — our go-to “savings account” where we park idle capital pending deployment into higher-yielding strategies or private deals.

To counter this compression:

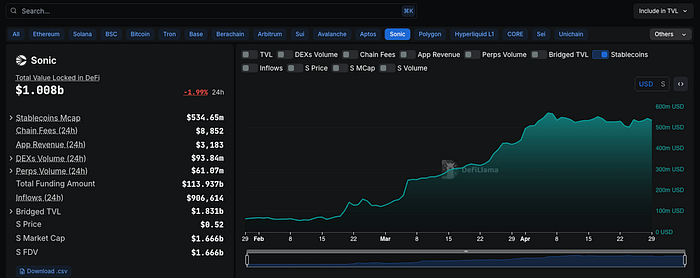

Since early January, we’ve actively deployed capital into advanced farming strategies on the Sonic chain, entering when stablecoin TVL was around $50M. TVL has since grown over 10x, and we expect a potentially significant airdrop in June.

Since February, we’ve also been active on Berachain, participating in hedged AMM strategies to mitigate volatility while capturing yields.

Lastly, many fund managers were caught off-guard when Usual adjusted the floor price of USD0++ from $1.00 to $0.87. However, at Sigil, we anticipated this development, as (a) USD0++ is not a stablecoin pegged to $1 but rather a four-year bond, and (b) the temporary peg was clearly outlined in the project’s documentation. Sigil Stable acted opportunistically, actively purchasing USD0++ around the $0.93 level.

Enhancing Counterparty Risk Management

As part of our ongoing commitment to risk mitigation and operational robustness, we are in the final stages of onboarding with Copper ClearLoop. This integration will allow us to diversify execution venues for our carry trades and hedged positions, while significantly reducing counterparty insolvency risk.

ClearLoop’s off-exchange settlement framework ensures we can retain custody of our assets while trading across multiple venues.

Q1 AUM Growth

Sigil Stable assets under management grew from $15 million to $23 million in Q1 — an $8 million increase.

This growth came from a mix of new individual and institutional investors, as well as existing Core fund investors looking to diversify into a market-neutral strategy. We believe it reflects growing interest in stable, uncorrelated returns during a volatile market environment.

We’ll stay focused on risk management, capital preservation and steady performance.

—

In the next quarterly letter, we will hopefully be able to dedicate more of the writing space for inspiring news within crypto. We love to discuss macro and politics like anyone else these days, but the core of our business is still to invest in disruptive opportunities in crypto and provide balanced exposure across all the most promising segments in the blockchain industry.

On the operational side, we decided to open up more of our decision making and thesis creation process to public articles. Apart from our quarterly letters, you can also look forward to more irregular articles covering some of our investments, strategies and opinions.

Thank you for your ongoing trust in Sigil Fund.

—

If you’d like to discuss your investment in Sigil Fund, please don’t hesitate to reach out to us at info@sigilfund.com.