Q2 2025 was in many ways more eventful for Sigil than the first one. Let us dive into it!

In Q2 2025 Sigil Core returned:

- 42.56% net of fees against EUR

- 55.3% net of fees against USD

…and beat the BTC benchmark by 19.61% net of fees:

In the previous letter I spent a lot of time commenting on global geopolitical events and even made some loose predictions, expecting armed conflicts to keep escalating. I wish I was wrong but that wasn’t the case. Israel enacted a series of attacks against Iran, decimating its military capacities, leadership and nuclear program. Iran of course retaliated and the conflict briefly escalated by the US bombing Iranian underground nuclear facilities. After this event, conflict somewhat de-escalated.

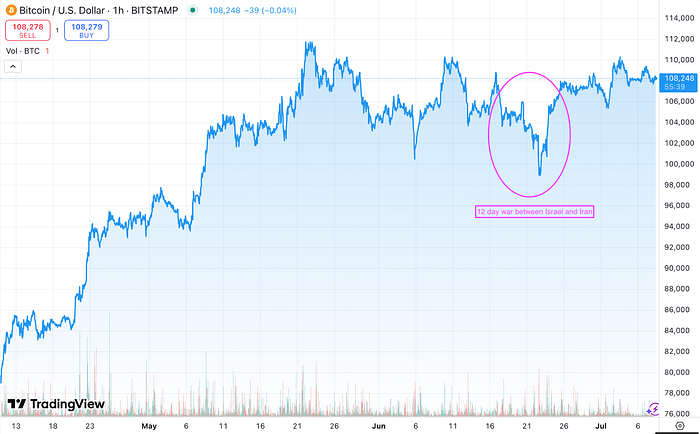

The markets reacted to this uncertainty by increased volatility short term, but ultimately they shook it off. Based on this, we may assume that the continuous tensions in the Middle East are already somewhat priced in and don’t pose an unexpected “Black Swan” risk. We can clearly see this both on Crude oil and Bitcoin price charts. The 12-day war between Israel and Iran ending with quite impactful involvement by the US is somewhat reflected on both charts but in the grand scheme of things, it’s just a volatility blip.

https://www.tradingview.com/chart/IsfNyfZ7/?symbol=BITSTAMP%3ABTCUSD

https://tradingeconomics.com/commodity/crude-oil

Another thing we previously focused on was Trump’s tariff war. During Q2 we didn’t see much impactful news, as the tariffs were put on a 3-month break which was supposed to end July 8. Perhaps not surprisingly, Trump extended the deadline again. My base case going forward is that rather chaotic tariff rhetorics will resume. Some countries will strike a deal with Trump, while others will become hardliners and escalate the economic tensions. Just as with the middle east tensions, we can assume markets are somewhat pricing the tariff uncertainty in, but we may still see increased volatility. Global supply chains and international business will need to adjust to tariffs. Prices of certain goods will be affected and largely transferred to the end consumer but ultimately markets will find a way to absorb this shock and keep on going.

With the global political commentary out of the way, we can now focus on events in crypto. In the second quarter there is a lot to report on.

Circle — IPO success

First and foremost, one of our biggest wins of this cycle — Circle IPO, which was extremely successful by any merit. We have covered it in detail in a separate article. During the time of writing this article (07.07.2025), Circle stock trades at around $207 and it is one of our biggest positions in Sigil Core.

https://www.tradingview.com/chart/IsfNyfZ7/?symbol=NYSE%3ACRCL

Sigil Core invested in Circle in an OTC transaction last year for the price of around $22 per share, so it currently sits on quite substantial unrealised gain. It is important to note that Sigil Core is part of a shareholder group that is locked for 6 months post IPO. That means we are contractually bound to not sell our shares or hedge them in any way before November 2025. This is fairly standard during most IPOs — original private shareholders get locked post-IPO for a certain time.

Please also note that Sigil Core currently applies a -30% discount to the fair market price of CRCL in the NAV. This approach is based on IFRS guidelines and NAV accounting principles. Due to the “decreased marketability” of the asset (we cannot sell or hedge at the moment) it is mandatory to create a DLOM discount (“Discount for Lack of Marketability”). Although CRCL trades publicly, our investment remains under a lock-up that materially restricts our ability to realize value. Effectively this means that:

- If the market price of CRCL is $200, our valuation is only $140 in the fund NAV so far.

- Once the IPO lock period expires the discount will disappear. We will also be able to sell or hedge the asset after the restricted period lapses.

Sigil Core as an investment vehicle remains fully liquid for our investors, who can deposit anytime and can withdraw their funds any time they see fit with a 5-day notice. We advise you to keep in mind the discount to CRCL stock in the NAV. To put it simply, there are 2 ways to look at this:

- Optimistic: Once the IPO lock is over, there could be a further upside to our NAV as the discount gets removed. Once the unlock expires, Sigil team will also have the ability to actively manage the position as we deem appropriate.

- Pessimistic: CRCL is already now quite volatile and it’s likely there could be some sell pressure on the unlock. The discount protects our investors from the potential adverse impact to the NAV.

Our fiduciary responsibility requires us to reflect all known constraints on the asset liquidity. While CRCL has appreciated significantly post-IPO, our shares are subject to a 6-month lock-up. Accordingly, and with the fund administrator’s approval, we have applied a 30% valuation discount to make sure the fund NAV is true and fair.

That is not to say we are bearish on Circle, quite the opposite. Of course, it’s reasonable to claim that the price went a bit ahead of the underlying fundamentals if we look at the snapshot in time. However, Circle is currently entering a supercharged growth phase with lot of tailwinds and bullish news:

- GENIUS Act provides positive regulation for adoption of stablecoins

- Circle applies for Banking License

- Institutional onramp for USDC and EURC

- Circle is one of the most profitable crypto businesses with growing market share

- Circle Payment Network is tackling cross-border payments

- Big tech companies pushing for stablecoin integrations

From the flurry of positive news around Circle post-IPO, it’s obvious the company is working hard to establish itself as a leader not only in crypto, but in the financial and big tech world. It also becomes clear that Stablecoins are a major innovation. They are to crypto as LLMs are to AI — a significant breakthrough that shows global product market fit and rapid growth. Thus, betting on stablecoin adoption is not a risky proposition anymore.

The risk now lies mostly in Circle’s ability to wrestle market share against its biggest competitor Tether and against incumbent traditional banks, who are scrambling to enter the arena. Circle definitely has an edge against their competitors. Arguably it has a more solid reputation than Tether, which is considered to be an integral part of the global shadow economy. It also has a significant technological and adoption headstart against traditional banks which need to overcome technical debt of their 50 year old systems if they want to adopt crypto infrastructure.

In conclusion, while our large Circle position remains locked for another 5 months, it’s still a very good problem to have. We are proud we were able to offer this unique exposure to our investors. While we cannot de-risk our Circle position yet, we discount the locked position by 30% so that the NAV gives a true and fair view. We then leave it up to our Core investors themselves to decide whether they wish to de-risk their exposure and e.g. move part of their portfolio cost-free to the Sigil Stable fund — or if they see the future discount removal as an opportunity to stay long.

While we are constantly searching for similar winning opportunities, we are seeing more and more crypto companies filing for IPO to capitalize on the success and hype around Circle. Most of them are, however, opportunistic and we don’t expect them to do nearly as well as the first mover, therefore we advise caution investing in those.

Hyperliquid’s strong performance

Another big winner of Q2 in our portfolio is Hyperliquid. We mentioned this project multiple times in the past few letters as one of our biggest high conviction bets in DeFi. In Q2 our thesis keeps being validated with HYPE (Hyperliquid’s native token) bringing outstanding price action of around 300%. Sigil Core derisked part of the position at around $35 level as we believe the project is now more or less fairly priced. We continue to ride the rest of the position for future growth as Hyperliquid continues dominating the DeFi perpetual contracts market, having over 80% market share at the time of writing. HyperEVM ecosystem and HIP-3 (improvement proposal for Hyperliquid to solidify itself as a go-to on-chain exchange infrastructure) are other potential vectors of future growth.

https://www.tradingview.com/chart/IsfNyfZ7/?symbol=PYTH%3AHYPEUSD

Robinhood’s ambitious plans

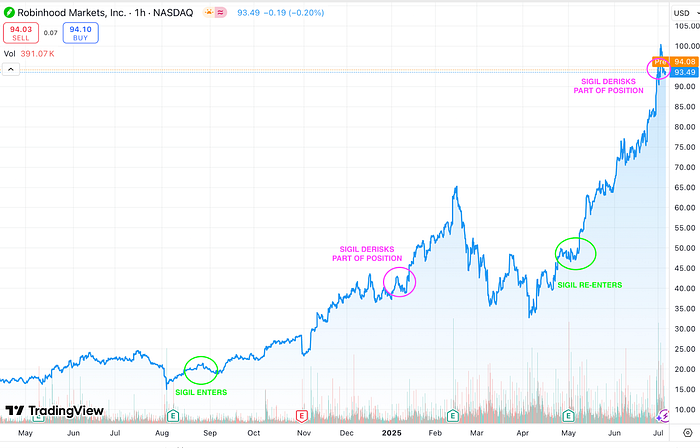

Our next big winner in Q2 is another Sigil Core stock position — Robinhood (HOOD). Unlike most of our investments which are largely crypto native, Robinhood is an established TradFi company, offering access to a variety of traditional markets to predominantly US retail audiences.

We invested in Robinhood in Q2 2024 after we spotted their first plans to move a big part of their business focus into crypto. Recently their crypto plans became much more crystallized. Robinhood acquired crypto exchange Bitstamp, introduced perpetual futures and announced building their own L2 which will be used mostly for tokenisation of stocks and select pre-IPO shares.

Vlad Tenev’s presentation during the Ethereum conference in Cannes caught the attention of the global crypto community. Translation from Chinese: “Robinhood is going to bring the entire financial world to the blockchain!”

Currently we believe the crypto news around Robinhood is already priced in and now markets will wait for the quality of their execution. That’s why we decided to significantly derisk our position while keeping a big part of potential upside as we believe Robinhood can become a major crypto player in the next 1–3 years.

https://www.tradingview.com/chart/IsfNyfZ7/?symbol=NASDAQ%3AHOOD

Coinbase exit

Lastly, we fully exited our Coinbase (COIN) position. We have been invested in COIN since May 2023, where we entered around the $50 price level. We were managing the position relatively actively but held the bulk of it until June 25. We decided to fully exit for 2 main reasons:

- Circle has a revenue sharing joint venture with Coinbase, sharing around 50% of its revenues with Coinbase. Now that Circle is publicly traded, CRCL and COIN are becoming correlated. Since we couldn’t derisk our CRCL position, we decided the next best way to derisk our exposure is to sell our COIN position. We also expect to see attempts to renegotiate the revenue sharing agreement with Coinbase, although this is a controversial view and we don’t expect it sooner than mid-2026. According to our analysis, such renegotiation may prove difficult.

- Coinbase product execution is often lacking, especially compared to their stiff competitors such as Binance and recently also Robinhood. Their gigantic data breach and lacking customer support point towards potential internal issues and overextension.

That being said, we still believe Coinbase is a great company with a lot of potential and we will keep watching their progress closely.

https://www.tradingview.com/symbols/NASDAQ-COIN/

Observant readers might have already noticed that in this letter I am focusing on stocks more than cryptocurrencies and tokens. Stocks are indeed dominating the crypto industry. Please note that this is not an invalidation of crypto, quite the opposite. I view it as an important milestone, a sign of crypto maturing and coming to terms with the larger business world outside. Some digital assets will keep providing differentiated investment opportunities, others will increasingly resemble stocks and some traditional companies will start using blockchains and crypto to gain an innovative edge against their peers.

Hegel’s Dialectic: Synthesis is upon us — crypto enters a new phase of legitimacy and adoption.

Crypto treasury companies

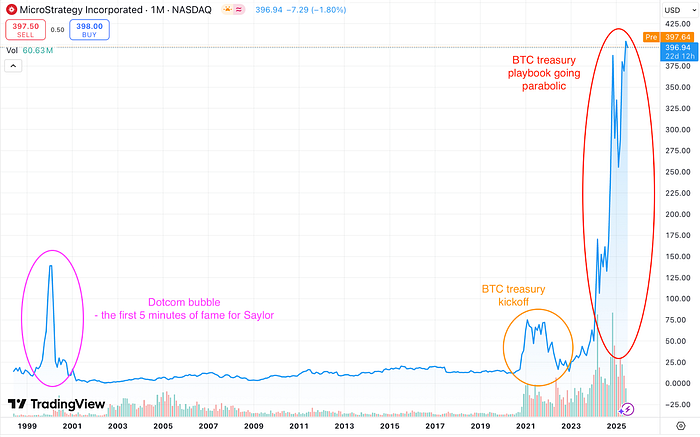

One of the hallmark signs of these two worlds colliding are so-called Treasury Companies. The first and most successful one is Strategy (MSTR, former Microstrategy). It used to be a failing publicly traded software company, until the founder and CEO Michael Saylor decided to pivot and leverage the fact he had a publicly traded company to create the first Bitcoin Treasury company.

https://www.tradingview.com/symbols/NASDAQ-MSTR/

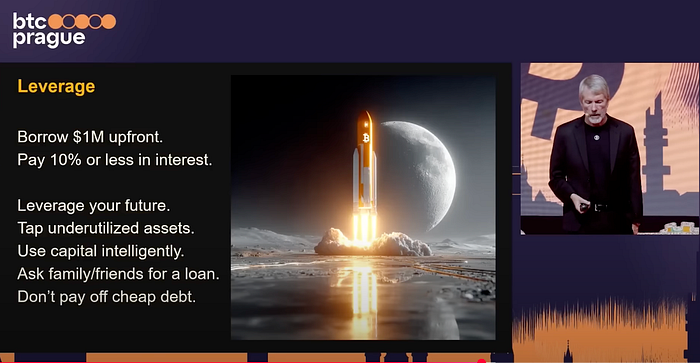

Strategy essentially transformed its corporate treasury into a Bitcoin investment vehicle. In simple terms, the company used its cash to buy Bitcoin and hold it on its balance sheet instead of holding traditional assets. Additionally, it raised more money to buy Bitcoin both via issuing more debt (mix of senior convertible bonds with various maturity dates) and shares (via at the market offering). This unconventional playbook has turned Strategy into a structured proxy for Bitcoin’s performance. Investors can choose from a variety of products that reflect their own risk appetite. Some of the products are viable also for credit investors who couldn’t touch Bitcoin exposure otherwise. The financial alchemy behind Strategy is somewhat complex — Saylor claims he used AI to come up with it. In its essence, Strategy is making a bold, long-term bet on Bitcoin’s continuous growth.

Saylor himself is a very charismatic character, who knows how to talk to both the institutional corporate world and Bitcoin community. I had the pleasure to attend one of his famous talks at the BTC Prague conference. The experience can’t be described in any other way than cult-ish. From chanting crowds to Saylor’s black dress with white Bitcoin logo resembling a preacher’s attire, all the way to his grand Bitcoin “prophecy” (sic).

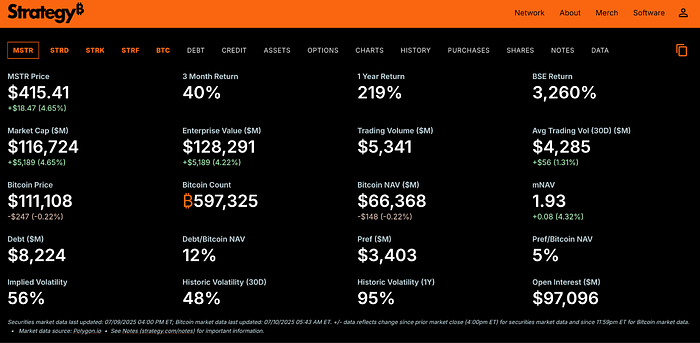

The sermon…uhm I mean presentation… was recorded, so you can watch it and draw your own conclusions. Cultish vibes or not, Saylor’s playbook reaped huge success and Strategy now holds almost 600k BTC on its balance sheet ($65 billion at the time of writing of this article — July 8). Currently MSTR market cap is 116bn, which means it trades with a 93% premium to its Bitcoin treasury NAV.

While this may sound irrational, this premium exists for multiple reasons. Markets are betting on Saylor’s continuing ability to issue various types of products in order to accumulate more Bitcoin. As BTC price grows, it also improves Saylor’s ability to keep issuing more products and accumulate more Bitcoin. We call this “a flywheel effect” or “a positive feedback loop”, where growth begets further growth. We have seen this happen a few times in DeFi as well, and let’s just say it is not always sustainable, but for now the music continues so everyone dances. It may very well be the case that Saylor’s Strategy is a special snowflake and they will be able to transition into a sustainable Bitcoin Structured Investment Product Company (almost like a proto-investment banking company).

Strategy provides a neat dashboard with all of the important KPIs for all of their products on their website.

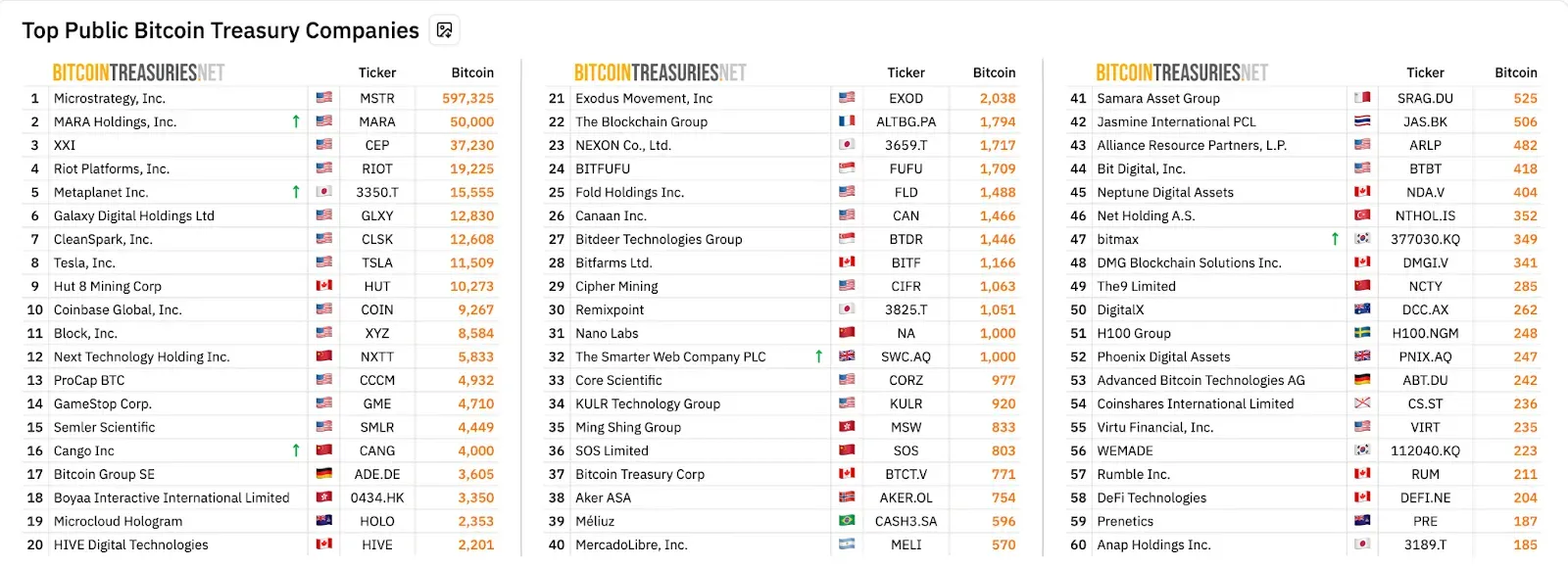

Unsurprisingly, Saylor’s success inspired many copycats. There are now more than 200 publicly traded companies doing essentially the same thing - offering various levels of risk:reward exposures to various types of investors by accumulating digital assets into their treasuries and then issuing stocks and debts against it with varying terms.

Top 60 BTC treasury companies, source (Please note not all of these are doing the full Strategy playbook, some, like Tesla simply decided to acquire BTC as a diversification to their cash reserves).

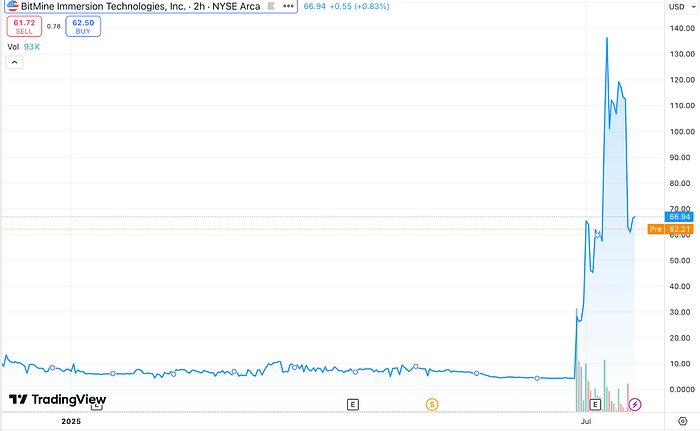

Most of these treasury companies focus on BTC. But there are some aiming to accumulate ETH, SOL, XRP or even HYPE and more exotic assets. Notably, Joseph Lubin (influential Ethereum investor and Consensys founder) acquired a publicly trading gaming company Sharplink Gaming (SBET) to run a similar playbook to Strategy with ETH as its chosen asset. ETH was also chosen by well known analyst Tom Lee (fundstrat.com) who joined the board of Bitmine (BMNR) to do the same.

https://www.tradingview.com/chart/?symbol=NASDAQ%3ASBET

https://www.tradingview.com/symbols/AMEX-BMNR/

Market reaction was very…volatile for both of these stocks

While it’s good to see all these players are bringing crypto closer to institutional and mainstream investors, I also need to issue words of caution. Most of these companies trade with a significant premium to their NAV and in many cases it is not justifiable with any sort of innovation or differentiation. While Strategy premium may become sustainable over the long run if they keep innovating and leveraging their brand and first mover advantage, I believe most of the other treasury companies will eventually end up trading with a discount to their NAV.

This may lead to a situation where shareholders start exerting pressure on the board to liquidate the company and sell off the treasuries. Some of these companies may even become a target of hostile takeovers. To prevent these risks, management may choose to sell off crypto in the treasuries in order to buy back their stocks and it can create a vicious, negative feedback loop. I personally do not think that this risk is imminent, and some of my colleagues in Sigil disagree that it is a significant risk at all, however it is always useful to think about bearish scenarios in the face of a hyped mania.

This was a complex topic, so let’s recap:

- Some publicly traded companies decide to hold part of their cash reserves in crypto, while others are the true “Treasury Companies”. These companies buy crypto and then package it into various financial products in order to attract different types of investors with differing mandates and risk appetites.

- This creates a positive feedback loop that propels crypto prices and enables more of these companies to accumulate more crypto, issue more stocks and debt, but there is a risk this flywheel will reverse in the future and many of these entities will be forced to sell and close shop.

Note: As of the day of writing of this letter (July 8, 2025), Sigil Core doesn’t hold any stocks of crypto treasury companies but we do hold underlying assets such as BTC, ETH, SOL which directly benefit from the buy pressure by these companies.

ETF flows

Another group of financial players we are observing are crypto ETFs. In Q2 we have seen positive inflows into both Bitcoin ETFs and Ethereum ETFs . It is worth noting that big part of BTC ETF inflows is matched with equal spot selling, which indicates that many Bitcoin holders are simply selling their BTC to buy BTC ETF in order to mitigate their self custody risk among growing hacks and financially motivated physical attacks and kidnappings of prominent crypto figures.

Q3 outlook

Looking forward into the Q3, there are multiple things to pay attention to. I already mentioned continued tariff and macro uncertainty, but that’s being baked into the market prices already. In crypto we expect a couple of interesting events. One of the most profitable and controversial crypto projects of this cycle, Solana based memecoin platform pump.fun announced an ICO (Initial Coin Offering) aiming to raise record breaking sum. Initial estimates point towards >$1bn, a sizable warchest which the team aims to use to grow their product and “kill TikTok, Facebook and Twitch”.

World Liberty Finance — a DeFi protocol connected to Donald Trump recently passed governance vote indicates that their native token WLFI could become tradeable in the next few months. Given the continuous attention around Trump and anything he does, we expect this token launch to be heavily publicised as well.

Lastly, Plasma — a bitcoin based payment network closely connected to Tether — is also expected to launch their token in Q3. Given the dominant position of Tether on the market we expect to see a lot of hype around this event as well.

So far it looks like Q3 is going to be an exciting time for crypto markets, with plenty of high profile launches. It goes without saying that we are closely monitoring these and other opportunities and will position ourselves to give our investors the best exposure. Sigil Core remains almost fully allocated with over 90% of portfolio risk on. We also do not plan to manage our risk exposure very actively as our investors are encouraged to reflect their own risk appetite by splitting their exposure between Sigil Core and Sigil Stable.

Sigil Stable Q2 2025 update

In Q2, Sigil Stable delivered a 3.01% net yield after fees (CAGR: 12.8%) for our investors, with a Sharpe ratio of 3.25. Our year-to-date CAGR stands at a strong 18.14%.

Our BizDev efforts were highly effective in Q2, as reflected in our GNAV chart. Assets grew by nearly 50%, from $23.1M to approximately $32.8M. Net inflows into the fund totaled $8.8M.

This growth came from a mix of new individual and institutional investors, as well as existing Core fund investors seeking to diversify into a market-neutral strategy. We believe it reflects the increasing demand for stable, uncorrelated returns in a volatile market environment.

Please note we normally don’t report the AUM in public reports but as Sigil Stable is at its inception (it opened to external investors in 2025), we feel the quick growth to a reasonable size ($100m+) is an important indicator. Larger fund allows for more stability and is easier to enter for bigger investors from TradFi and the likes.

OTC Discounted Deals

In Q2 we worked hard on researching new opportunities to buy discounted tokens OTC. Despite the due diligence work done we didn’t enter any new discounted token position, though. It is a good thing. Let us explain why.

As some of you already know the OTC discounted deals may be very profitable for Sigil Stable, when done right. The general idea is:

- You buy a token on spot with a discount (LONG leg of the neutral position); AND

- You hedge partial or full exposure on some of the centralised or decentralised exchanges with a SHORT position.

- As you enter the position with the discount you are guaranteed to make a profit regardless of the price movement.

- Sometimes you even make a “double dip” profiting from the funding rate on the short position (when “longs pay shorts” on the perpetual futures market). However, it is crucial to be very picky about which tokens we buy because if the project is not great, the funding rate can turn very negative (“shorts pay longs”) which can reduce our profit. Poor quality tokens could even be delisted from the exchanges. In such a scenario you could end up holding a long position in a “shitcoin” without the ability to short it.

That’s why we are extremely picky about which opportunities we enter. Ideally we work with high quality tokens where the discounted deal is rare and available only to well established high profile funds.

In Q2 there were a few examples how some investors, even large and reputable ones, did it wrong and took a hit. It usually starts with an attractive discount. If the discount is too good or is offered everywhere (we are well connected in the space so can evaluate this), it is usually prudent to stay out.

Such was the case with Aza Ventures which turned out to be the largest OTC scam operation in the discounted deals. Crypto funds and HNWIs were initially lured with legitimate deals that helped build trust. Once confidence was established, the scammers scaled up their operations, ultimately defrauding investors of approximately $50M through subsequent deals.

Thanks to our due diligence efforts, we didn’t participate in any of the dubious deals. In addition to this, we also avoided a high-profile deal that attracted many other Tier 1 funds. While in the final stages of negotiating the deal, we were privately alerted by a well-respected industry figure to what we’ll diplomatically call “crypto shenanigans”. The information we received, concerning the founder of the project, had not yet been made public (though it surfaced a few days later), but it was serious enough for us to walk away from the deal before any legal contracts were signed.

This experience served as a valuable reminder: in crypto, being hands-on and well-connected isn’t optional, it’s essential. Sigil remains one of the longest-standing liquid crypto funds, with its flagship fund Sigil Core operating continuously since 2018.

Sigil did not participate in any of these “opportunities,” as we work exclusively with the most experienced brokers or directly with project teams and foundations.

Yield Farming & Airdrop Strategies

Our May performance was primarily driven by the Berachain BOYCO airdrop, distributed based on activity over the prior three months.

Our strategy involved borrowing ETH and WBTC using USDC as collateral on Aave, the largest money market. We then pooled the borrowed ETH and WBTC in a Uniswap V2 fork on Berachain. This approach yielded more than double the returns of a typical stablecoin AMM pool even after accounting for impermanent loss (which became realized upon exiting the position) due to ETH’s underperformance relative to BTC.

On-chain TVL dropped significantly, from $2.4B at the time of BERA incentive distribution for the BOYCO liquidity unlock, to $400M by the end of Q2.

Clarifying Our Approach to Market Neutrality

Looking ahead, we want to clarify how we think about market neutrality at Sigil Stable. The approach is: Sigil Stable is market-neutral most of the time and always market-neutral in terms of 90% of the portfolio. But there are specific, carefully considered cases where we are not 100% market-neutral. Let us elaborate.

The main reason we might temporarily accept directional exposure is to access asymmetric opportunities where real or implied yield meaningfully outweighs tail risk.

A good example is the Plasma raise (also mentioned in the Sigil Core section of this letter). Plasma is a volatile token with full unlock at TGE (Token Generation Event). To gain access, we needed to provide stablecoins, effectively a function of time and size, to earn the right to invest. Based on our research, the opportunity was a no-brainer.

We were prepared to allocate the maximum 10% of NAV allowed by our guidelines into a stablecoin vault. The vault would deploy capital into Aave and subsequently bridge USDT to the Plasma chain. In return, we would receive an allocation right of roughly $150k in Plasma tokens at a $500M fully diluted valuation, with tokens fully unlocked at TGE. At the time, we projected a $2B valuation — implying a 4x return.

Our thesis appears to be playing out: as of this writing, Polymarket odds for Plasma trading above $2B are at 80%.

The deal attracted huge interest. Such was the demand that one depositor paid over $100k in gas fees to get in. This time we were able to allocate a small amount using our on-chain bot — but on a positive note, we’re now better equipped going forward. Being able to identify highly profitable opportunities, together with utilising our new on-chain bots, puts us in a strong position to secure similar deals in the future.

Another case where Sigil Stable may experience limited market exposure is in volatile AMM pools, those where at least one asset (e.g., ETH/USDC) is not a stablecoin.

While we hedge these positions, pool composition naturally shifts with price changes. When the price of the volatile asset drops, the pool ends up holding more units of it. If our short hedge isn’t large enough to fully offset this, we’re left with a partial naked long. Conversely, when prices rise, we hold fewer units of the volatile token, and our short becomes oversized, resulting in a partial naked short.

There is no bulletproof way to be perfectly hedged across all price ranges.

One illustrative case is our INIT/USDC 80/20 weighted AMM pool, initiated in May. We entered the position with INIT exposure fully hedged via perpetuals, and the strategy initially delivered above 100% net APR. However, following a sharp decline in INIT’s price, we found ourselves with a partial naked long, as described above. This slightly impacted our June performance.

That said, we fully exited the position in early July. The final PnL was positive.

Q3 Outlook

At the end of Q2, we signed a private liquidity deal with a highly anticipated stablecoin project backed by AI hardware. We allocated 10% of NAV to this opportunity, alongside participation from top-tier crypto and TradFi funds.

Looking ahead, we expect to participate in at least one opportunity similar to the Plasma deal described above and are currently working on several additional OTC deals.

Most notably, we will be launching both our on-chain and off-chain trading bots, which have been in development and testing since Q1. We believe these bots will help us unlock a new strategic vertical for Sigil Stable.

Thank you for your ongoing trust in the Sigil fund.

—

If you’d like to discuss your investment, please don’t hesitate to reach out to us at info@sigilfund.com.