Dear Investors,

In the third quarter we saw an increasing optimism on the market, sparked by potential Bitcoin (and Ethereum) spot ETF approvals. The overall macroeconomic situation stayed pretty steady. To sum it up, the past quarter felt like the calm before a bullish storm in the crypto market. Let’s explore these recent changes in more detail.

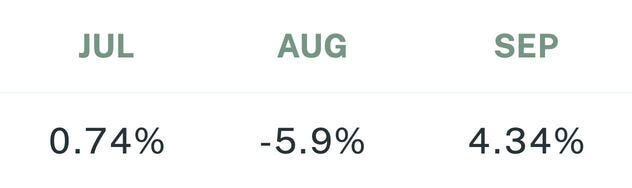

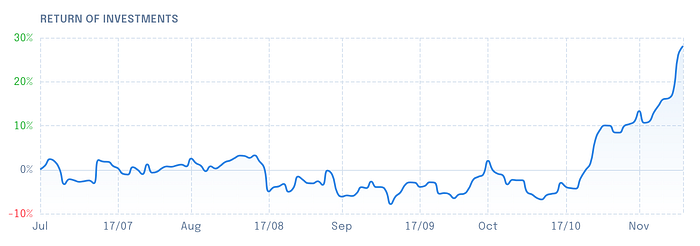

In the Q3 of 2023, Sigil Core recorded -1.09% vs EUR, -4.14% vs USD, +8.34% vs BTC.

Sigil Core Net Performance vs EUR Q3 2023

Crypto ETFs (Exchange-traded funds)

Bloomberg analysts estimated a 75% chance of a spot Bitcoin ETF being approved in 2023 and 90% by January 10, 2024. This milestone gained additional momentum as the largest asset manager, BlackRock, secured a ticker symbol for its upcoming spot Bitcoin ETF

The positive expectations around Bitcoin ETFs, started to shift market sentiment towards a bull phase of the crypto cycle. If you haven’t read the in-depth Sigil CEO’s article on these topics, you should do so here.

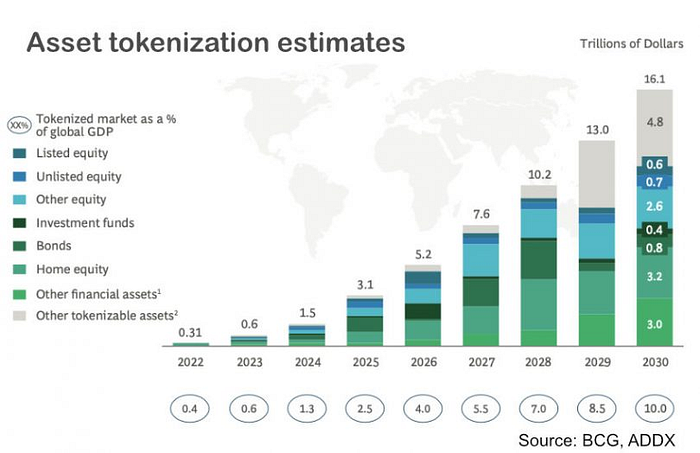

Real World Assets

Real World Assets (RWAs) experienced a surge in popularity. RWAs are basically tokenized tangible assets brought onto the blockchain with various technological and legal wrappers. Among RWAs, stablecoins like USDT and USDC stand out as the most widely used in the crypto markets. These are crypto tokens designed to maintain a value equivalent to 1 USD, backed by real dollars in the bank or similar financial instruments held by their issuing entities. Some even allow direct redemption for dollars, ensuring the stablecoin’s value remains pegged at 1 USD. Currently, one of the significant applications for stablecoins is in payments and exchange settlements within the crypto space.

Other examples of RWAs include:

- Precious metals (such as Tether Gold — XAUT)

- Commodities (wildest example being Uranium backed token U)

- Art (famous artist Damien Hirst used NFTs as his new medium of expression)

- Real estate (tokenized and fractionalized such as at Landshare)

- US Treasuries (Ondo OUSG offering iShares Short Treasury Bond ETF)

Press enter or click to view image in full size

Why would we even bother tokenizing assets existing outside of the blockchain?

- Lower barriers for financing, especially in emerging markets (Goldfinch, offering liquidity pools for microloans in developing countries)

- Lower entry barriers for retail investors or consumers (in many developing countries, stablecoins are the only way to access exposure to USD)

- Better capital efficiency through faster settlement and automated execution (it takes minutes to settle an on-chain transaction)

- Lower operational costs

- Transparency (blockchains are public and immutability, enabling anyone to independently verify the data without trusting a third party)

- Composability as tokenized assets can be further utilized in DeFi

In Sigil’s portfolio, Canto, originally a general-purpose Layer 1 blockchain converted to an Ethereum Layer 2. This choice aims to leverage Ethereum’s deep liquidity, allowing Canto to evolve into a protocol focused on real-world asset tokenization.

Coinbase

After successfully booking 1 ⁄ 3 of the profits from the COIN (Coinbase stock) position, as highlighted in a previous letter to investors, we have again increased our position, taking advantage of local price lows around $70. In Q3 Coinbase revenues managed to beat analyst estimates. Coinbase generated $674.1 million in revenue during the third quarter of 2023 compared to $590.3 million for the same period in 2022.

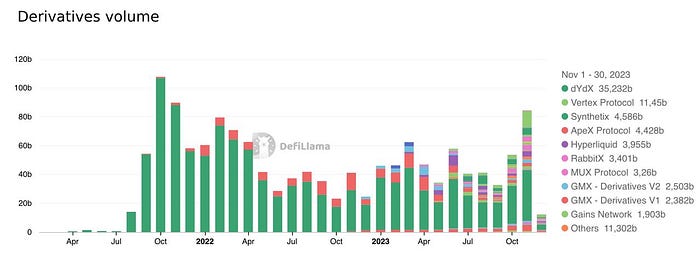

DeFi (Decentralized Finance)

The DeFi segment has been underperforming, despite DeFi being one of the cornerstones of crypto adoption. We see many DeFi protocols expanding across verticals to capture the most market share. Instead of “money lego thesis”, where we expected DeFi protocols to become composable and complementary to each other, we see a fierce competition. We positioned our portfolio to reflect this new dynamic.

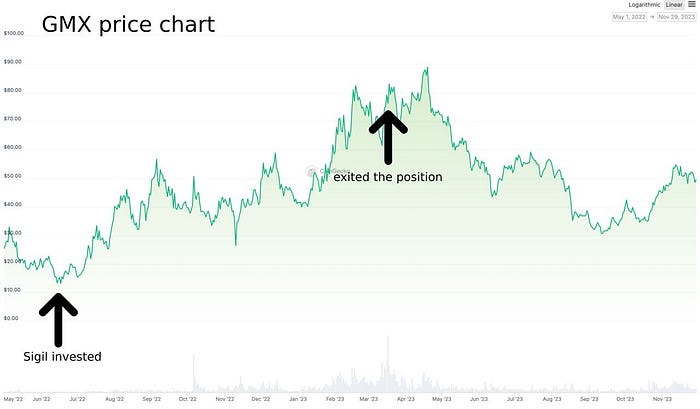

One DeFi segment seems to be an exception in performance — decentralized leveraged trading. We are well positioned to capture upside from this trend. Despite exiting our GMX position, we remain allocated and doubling down on two other market leading perpetual protocols — DyDx and Synthetix. Historically DyDx dominated market share mostly thanks to its incentives but recently we are seeing the DeFi perp market getting more organic volume and a more diverse set of competitors.

Our strategy going forward

Given the upcoming ETF approvals and halving in spring 2024, we have been allocating a significant portion of our portfolio into Bitcoin. While historically we did not have much Bitcoin in our portfolio, we cannot ignore the probability of BTC outperforming the market midterm, as it enables traditional investors to allocate into it via the instrument they know. We also expect the spot ETH ETFs to be approved in quick succession after the spot BTC ETFs. We assume the potential new money flows from traditional finance could lead to relative outperformance of Bitcoin.

Our plan is to reduce stablecoins in the portfolio to 0 and be 100% long allocated by the end of this year and re-evaluate our positions in Q1 and Q2 next year with new information. Of course, there is a possibility that spot ETF approvals for BTC and ETH are already priced in by crypto native players and they will become a “sell the news” event. However, mid to long term the new money flows from traditional financial institutions that will be unlocked by access to BTC and ETH via ETFs will be hard to ignore.

Investment opportunity

Because of the growth drivers and changing market sentiment, we’re seeing smart money already front-running the next boom phase of the crypto cycle. We are also noticing an increased interest from both existing and new investors of Sigil.

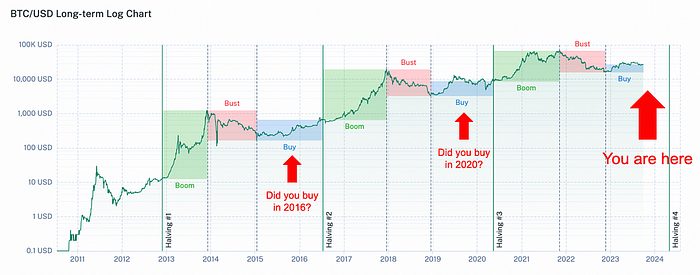

The question many of our investors ask is whether we will see another 4 year boom and bust cycle in crypto. Below, you can see the chart from the previously mentioned article by Sigil’s CEO, illustrating the past 4 year cyclicality.

While we do not believe history repeats, it very often rhymes.

Halving, ETF approvals, and potentially a more stable macroeconomic situation going forward could all lead to yet another renaissance for crypto. Many forward looking actors in crypto markets expect similar development, which could propel the 4 year cycle as a self-fulfilling prophecy.

On the other hand, markets have a way of teaching anyone who is too sure a hard lesson. Thus, we are also preparing strategies for a variety of different market outcomes. While we are fairly certain crypto prices bottomed last year and we are entering a bull cycle, it is possible this bull cycle will last much shorter or much longer than 4 years. The growth may also be a bit slower and more continual than in previous cycles, given the increased cost of capital. But we may also see the opposite — violent uptrend that will leave many slower investors sidelined.

Thinking probabilistically and calculating expected value from several possible market scenarios has always been one of our strengths.

Conclusion

What we’ve been signaling for the past two quarters is starting to materialize.

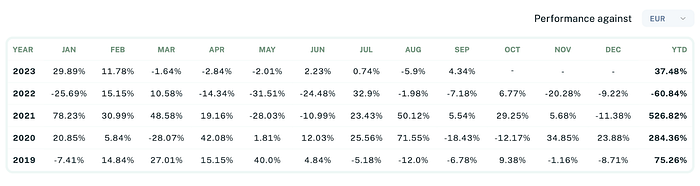

After 12 months since the last cycle bottom, BTC is +120% vs USD and the altcoin markets started warming up, too. Everything hints we are entering a boom phase in the crypto market with a positive momentum in the coming year(s). Boasting a strong track record of +264.98% vs BTC in the bull market year of 2021, Sigil is well-positioned to capitalize again on the coming bull market.

Thank you for your ongoing trust in Sigil fund.