Dear investors,

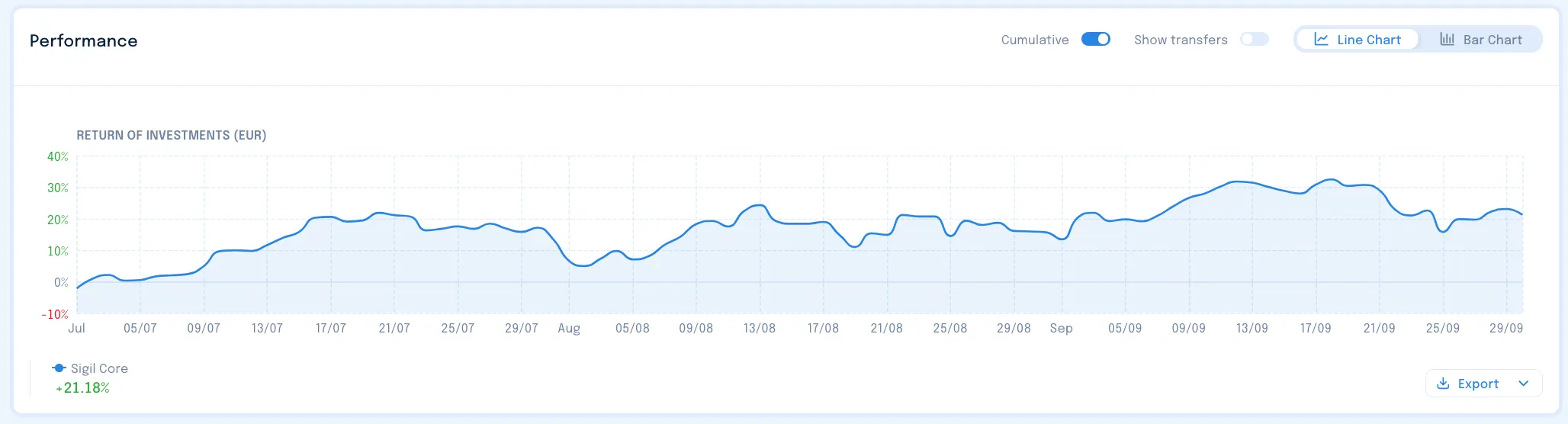

In Q3 2025 Sigil Core returned:

- 21.18% net of fees against EUR

- 20.68 % net of fees against USD

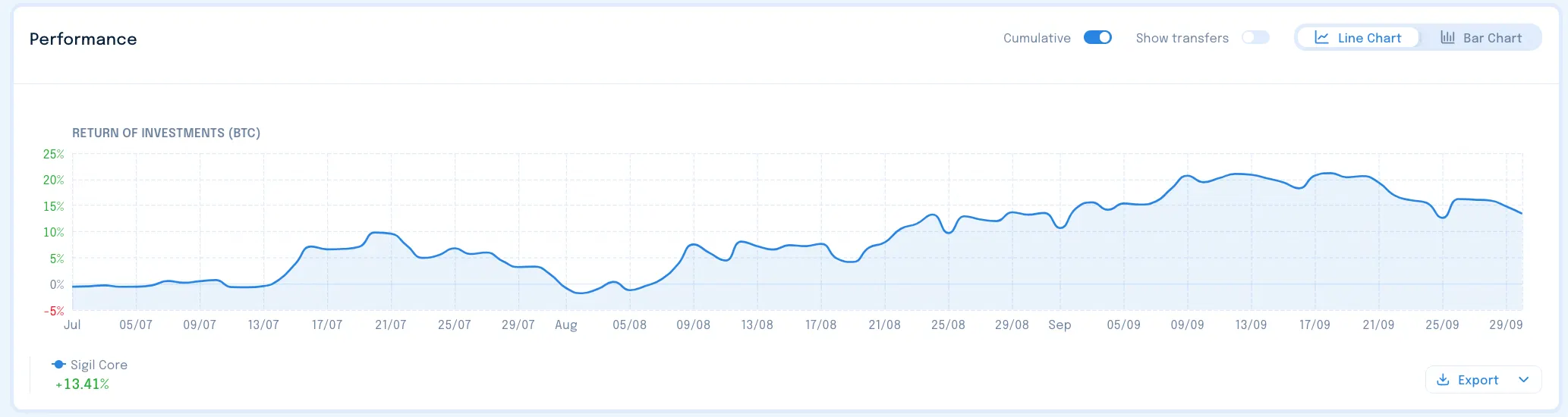

…and managed to beat BTC benchmark by 13.41% net of fees:

Crypto markets printed another fairly successful eventful quarter and it’s my pleasure to provide you with a fresh update. This update lands a bit later than usual. As we were wrapping the Q3 in early October we recorded two important events that warranted priority coverage — that is Polymarket up-round and record breaking liquidations in the market. These happened in Q4 but since many of you raised questions about these events, I will take the liberty to cover them already now, instead of letting you wait for another 3 months.

Polymarket repricing

Polymarket is a leading prediction market where users can bet against each other on a variety of different topics. It’s like sports betting but not limited to sports — you can bet on events ranging from global geopolitics all the way to culture, celebrities and influencers. Most of you probably heard of Polymarket in relation to providing odds for the US presidential elections.

The markets around these events are expressed as “odds” — e.g. markets approximations of probabilities, hence the term “prediction markets”. Not every user of the prediction market needs to be a speculator. Many journalists, experts and decision makers can refer to prediction market odds as a relevant source of news and information, often more accurate than e.g. polls.

Before Polymarket, there were a couple of early attempts at cracking this market, ranging from traditional bookies and platforms all the way to crypto native ones (Augur). However, it was Polymarket which was able to crack the code and deliver a successful prediction market as a high impact product. Over the last 30 days, Polymarket volume is over 2bn and recently they acquired a CFTC license which will enable them to open their product to the US customers. Sigil Core invested in Polymarket equity in December 2023 for the equity valuation of 125M USD. In October 2025 Polymarket closed its latest investment round valuing the company at 8bn USD pre-money — ICE (owner of the New York Stock Exchange) invested 2bn USD in Polymarket, giving it not only significant treasury to scale its business but also lending its legitimacy and business network in the US.

While another big success, our Polymarket investment in common shares is still illiquid and thus we are limited in our ways to manage it. Please note Sigil Core currently applies a -40% discount to the latest round valuation in the NAV because the position is completely illiquid while Sigil is a liquid fund with daily NAV. This approach is based on IFRS guidelines and the NAV accounting principles. Due to the “decreased marketability” of the asset (no public market where we could flexibly sell), it is mandatory to create a DLOM discount (“Discount for Lack of Marketability”). The discount also reflects the fact we have common stock from the early stage of the company while newer VC rounds were structured via preferred stock.

What does this mean for you? Three things:

- Sigil Core is a liquid fund so you can always withdraw money anytime, even if some of the positions are still illiquid. There was a nice performance boost due to the 8b ICE round in our NAV despite the -40% discount to that valuation we had to apply.

- If we manage to sell the position for a price that is higher than last round minus 40% accounting discount, Sigil Core fund will realise further performance gain.

- As a Sigil investor you can always view this from both possible points of view:

- As a long term holder you can hope for a further potential gain if we manage to sell higher than NAV valuation or if Polymarket goes through a successful IPO or if our token warrant leads to more liquid profits from the token or if the valuation just keeps growing higher. (all of these scenarios are of course speculative and the prudent valuation discount reflects it).

- Or you can decide to withdraw your money anytime knowing there was a nice markup in the Polymarket position. Yes, there is the discount but that fairly reflects the fact you can get liquidity from Sigil anytime while the fund still needs to work on realising the profit from the illiquid common stock position.

- The decision is always yours. Our job is to follow accounting principles, have the NAV approved by our licensed fund administrator and communicate transparently about it to our investors. It is also our job to make sure we always have enough liquid AUM to satisfy potential withdrawals of external investors (even if they withdraw all at the same time). We own roughly one third of our AUM and aspire to increase this to 50% over the coming years. One benefit for our investors is there is always enough liquidity for external investors to withdraw anytime.

Coming back from the bean counting to the high level investment point of view. We are extremely happy and proud we were able to give you exposure to Circle and Polymarket, both of which were one of the largest crypto successes of this year and contributed significantly to beating our BTC benchmark.

Record breaking liquidations

First of all, the most important question: How was Sigil affected?

Sigil Core uses leverage only to a very small extent and with very conservative parameters, at the time of liquidations it didn’t suffer any permanent loss of capital. However, Core holds long crypto exposure so, in this sense, it was indirectly affected by market price volatility.

With that out of the way — what actually happened? In the Q1 letter I mentioned we expected markets to be volatile thanks to the unpredictability of Donald Trump’s macro and geopolitical rhetoric. This has proven prescient in recent days, when Trump issued another strongly worded message against the Chinese. I would expect markets to already be used to such a thing, but we saw them overreacting again. This time however, the overreaction spilled into crypto and triggered forced liquidations of leveraged positions of gigantic proportions — around 19 billion USD of open interest was liquidated across both centralised and decentralised perp exchanges. It is still not known exactly why this happened, but it seems the issue originated on Binance, where multiple assets de-pegged and caused cascading liquidation events which spread to other exchanges. Binance later released the following statement and devised a plan to reimburse impacted traders to the tune of 700 million USD, which further points towards their systems being largely responsible for the crash.

Some altcoins have seen temporary crashes of 80% and in the case of ATOM it went basically to zero.

Perp exchanges triggered so-called ADL — automatic deleveraging — a last resort measure where traders positions are forcibly closed in order to prevent systemic risk becoming an existential threat to their business and market in general. The way these ADLs were conducted depended on the exchange. Notably, Aave (a DeFi platform) withstood the non standard situation without any hiccups. Hyperliquid, an on-chain competitor to Binance — also triggered their ADL. While many traders were forced to close their positions as well, overall the platform passed this stress test with flying colors. In our eyes, this event proved the superiority of open and publicly visible markets over a closed black box paradigm which centralized exchanges operate under.

While this liquidation event was record breaking in its size, it wasn’t really unique in its quality. Every cycle we see one or few of such deleveraging events and usually they present an opportunity to make a profitable trade by buying assets from forced sellers closing their leveraged positions. Thus, our reaction to this event was to use some of our dry powder to buy assets we deemed were over-sold with the plan to reconsider our positions after the dust has settled and new info has emerged.

On the other hand, we need to remain cautious. Many market makers and trading shops were hit hard in the event. The liquidations could have a short to mid-term negative impact on the crypto market structure as many of these traders will need to re-balance their positions to cover for their losses. Over the long run, however, this event made us even more bullish on open and robust market infrastructure built by projects such as Hyperliquid over closed and opaque legacy exchanges.

With commentary about the 2 special events out of the way, we can continue covering what else has been happening in Q3.

Ethereum and the ETHBTC trade

Q3 was a very interesting quarter for Ethereum and evaluating some of the long-term thesis around it. The PoS merge that happened in 2023 was the biggest and most awaited upgrade in Ethereum’s history. Most saw it as a huge bullish catalyst, reducing ETH inflation and switching from wasteful PoW (mining using hardware) to more efficient PoS (staking).

Ironically, ETH PoS merge basically marked the ETHBTC top and what followed was 2.5 years of miserable ETH underperformance vs BTC.

ETHBTC ratio price chart 2021 until Q3 2025. Source: https://www.tradingview.com/

This caught off-guard many investors, us included. With the benefit of hindsight there were a bunch of reasons why ETH was underperforming:

- Most crypto investors were overweight ETH, it was a consensus trade post-merge.

- Ethereum leadership (mainly Ethereum Foundation) was very lacklustre, inefficient and unwilling to divert resources from long term research to more business-productive endeavors (arguably still is, even though we see many improvements recently)

- Competing ecosystems such as Solana were able to capitalise on Ethereum’s weaknesses and carve out a significant market share

- Bitcoin had Michael Saylor and Microstrategy to make a ton of difference in the market structure of Bitcoin vs rest of crypto

- BTC ETFs launched earlier than ETH ETFs and thrived on institutional adoption.

- As BTC kept outperforming ETH (and most alts), the questions emerged whether the rest of crypto amounts to anything, or whether it’s all about Bitcoin (and maybe stablecoins). Questions like these usually mark a “sentiment bottom” as holders finally capitulate, enabling new fresh buyers to take their place

In Q3 2025 we finally saw signs that would give us a case for ETH to start outperforming:

- TradFi started getting more in tune with stablecoins and DeFi, looking for the best simplest exposure

- Circle and Coinbase were the best proxy bets for the stablecoin play but they quickly became expensive and ETH suddenly looked like providing more upside than these stocks (as ETH was still way below its previous all time high)

- Ethereum leadership started listening to community feedback and became more constructive

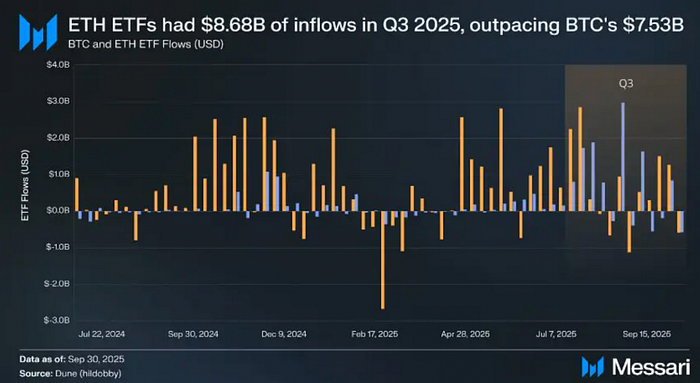

- Improvement in inflows into Ethereum ETFs compared to BTC

- ETH treasury companies emerged and promised a sustained buying pressure to mirror the MicroStrategy effect for Bitcoin.

ETH vs BTC ETF flows, source: https://messari.io/ and https://dune.com

Notably Bitmine (largest ETH DAT company) and its Chairman Tom Lee laboriously kept appearing in CNBC, Bloomberg and other financial mainstream media and pushing his Ethereum thesis to TradFi Boomers. For those interested, here is an ARK interview with him outlining all of his talking points about ETH (“ChatGPT moment for Crypto” slaps hard). Joe Lubin, man behind the second biggest ETH DAT SBET, issued his own bullish report on ETH.

We were waiting for confirmations of sentiment shift to rotate a significant portion of our NAV into ETH. While we don’t often use charts in decision making, here we decided to use ETHBTC momentum breakout to time the trade.

Currently, the momentum phase of the trade seems to be played out and we no longer hold as much ETH as in Q3. However, ETHBTC levels are stabilised above 0.035 and we believe if crypto bull run continues and Ethereum leadership keeps improving we could see ETHBTC ratio slowly grinding higher in Q4. Ongoing adoption of stablecoins by financial institutions, involvement of committed buyers such as Bitmine and EVM retaining its popularity as dominant DeFi environment will be key to ETH’s performance.

The Solana trade

SOL had a marvelous 2024 performance but in the later part of 2025 it started lagging behind. By the end of Q3 we saw a few Solana catalysts ahead:

- Formation of high profile SOL DAT company Forward Industries, led by heavy hitters — Multicoin Capital, Galaxy Digital and Jump Trading

- SOL ETF approvals likely in Q4

- Alpenglow — a Consensus upgrade making SOL more scalable and usable

- Concentrated push for Solana to become the Hub of “Internet Capital Markets”

We believe Solana’s biggest narrative competitor is Ethereum — currently Ethereum and EVM lead in institutional adoption but Solana is leading in retail and application adoption. Thus we decided to monitor SOL/ETH ratio and use it in a similar fashion to ETH/BTC ratio in our Ethereum trade.

Our mid-term SOL outperformance thesis will be developing into Q4 so we are not yet in a position to fully evaluate it. We will come back to it in the future.

Perp DEX wars

After the massive success of Hyperliquid (which we covered in previous letters), unsurprisingly many competitors emerged on the Perp DEX scene, promising airdrops and better, faster, bigger, stronger products. While most of these are mere copycats, there are few competitors worth mentioning:

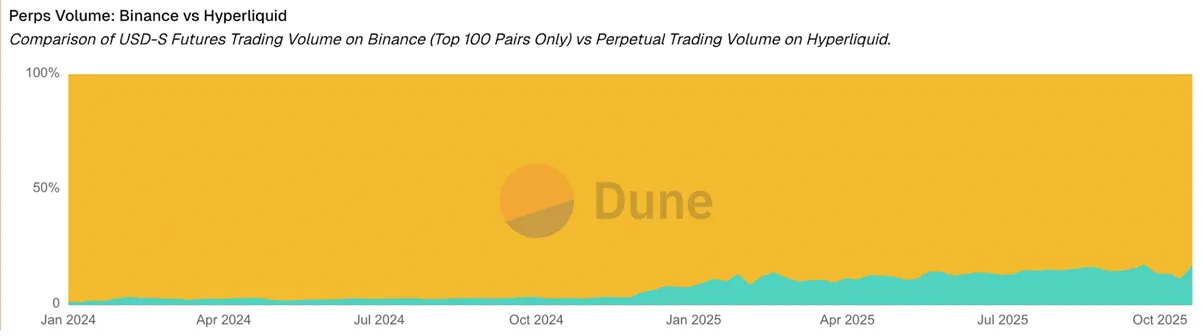

Aster is leveraging the vast resources, business power and infrastructure of its backer — Binance, which is using it as a proxy to re-capture market share lost to Hyperliquid.

According to Dune data, Hyperliquid perp volume is already at 17% of Binance

Lighter is a ZK layer 2 on Ethereum, promising fast and smooth user experience while inheriting Ethereum’s security guarantees. Currently it incentivises traders with point farming incentive system and zero trading fees.

Even our old love from DeFi Summer days — Synthetix — is reinventing itself with bringing Perpetuals directly onto Ethereum Mainnet.

With all the new Perp DEXes offering incentives and airdrop upside to traders, many unsophisticated market participants started using these products in order to farm the incentives and airdrops, partially contributing to the deleveraging event we commented on earlier. Now that OI was cleaned up from excess leverage, the Game Of Thrones for the best perp DEX can recommence. We are still betting on Hyperliquid to retain its lead, but we did open smaller sized positions in some of the other competitors.

In Q4 we expect many of the perp DEXes to expand their offerings from crypto to other assets such as stocks, commodities and indices in order to gain an edge.

Hyperliquid is well positioned to capture the lion’s share of these new markets with implementation of HIP-3 upgrade, which offers a permissionless way for anyone to utilise Hyperliquid infrastructure and build their own perpetuals for basically any market.

What to expect next

In conclusion crypto had a solid but not great Q3 (partially spoiled by the October liquidation). We are optimistic going into Q4 with many of the secular headwinds for crypto remaining in place. However we are also acknowledging increased frothiness across markets, notably AI related stocks and private equity. Even crypto VC rounds made an excessive comeback. Depending on the overall situation and price action we will be looking to partially derisk in Q4, while remaining flexible and ready to react to the fast paced crypto market environment.

On a general note, we need to make sure to not over-focus too much on the short term. While in times of heightened froth and uncertainty it’s often enticing to shorten one’s time horizon, we believe crypto finally entered a productive adoption stage, where winning use cases are much more clear and winning projects are starting to scale, develop moats and network effects. In this “winners keep winning” environment it will be easier to simply ride some fundamentally sound investments for longer. It will also be harder for new competitors to threaten the market share of the current winners. This situation will likely be analogous to the post-dotcom era of internet adoption, where giants such as Google, Facebook, Amazon, Apple and Microsoft were able to capture most of the upside and it was very difficult for new internet companies and internet focused VC portfolios to outperform these stocks for the last 20 years (unless you were in crypto). It remains unclear which titles will become the “FAANG of crypto”, but we have a couple of strong contenders in our portfolio. We remain fundamentally bullish on crypto trends long term and aim to consistently provide best exposure to its upside to our investors.

Probably the most frequently asked question from our investors is “Where do you think we are in the current crypto cycle”. First of all we’d like to emphasize that since Bitcoin halving becomes less impactful each time and crypto becomes more integrated into mainstream economy it’s far from certain we will have another clean four year cycle like we did in the past. However, if we assume the cycle is repeating itself, at this point we would definitely be in its late stage. We encourage our investors to swap their risk-on positions in Sigil Core for the market neutral Sigil Stable fund if they believe in the crypto (or macro) cycle theory and want to manage their risk exposure accordingly. Timing tops is impossible and booking profits when markets look frothy or you feel over-exposed is generally the best approach to personal risk management. More on Sigil Stable below.

Thanks for your ongoing trust in Sigil Core fund.

— Fiskantes and the Sigil team

Sigil Stable Q3 2025 update

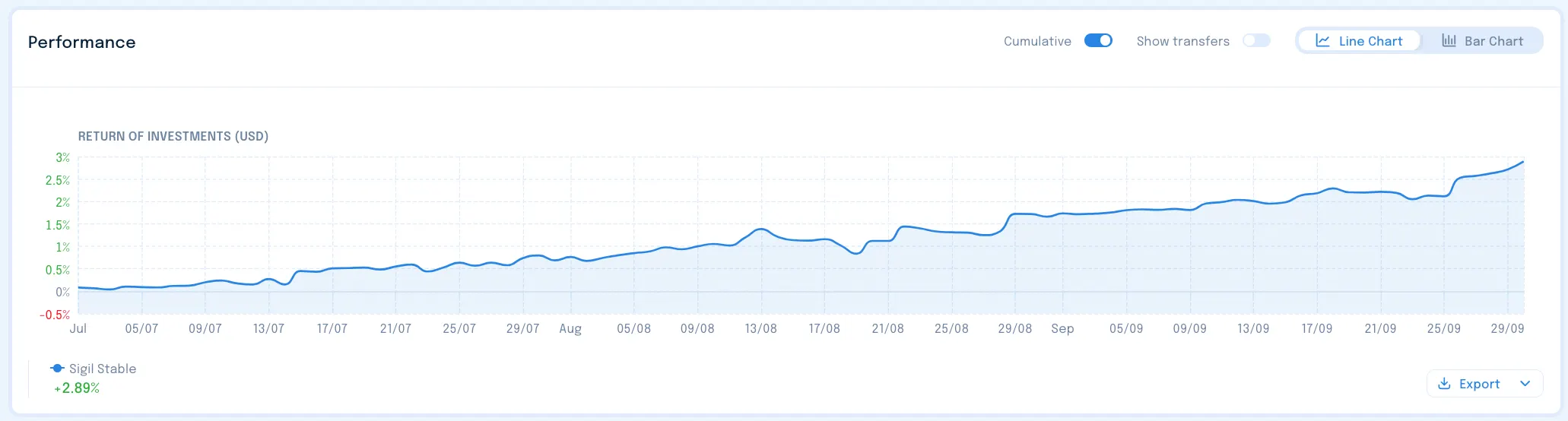

In Q3, Sigil Stable delivered (vs USD) a 2.89% net yield after fees for our investors, with a Sharpe ratio of 4.64

It was an eventful summer in the stablecoin world, with new yield-bearing tokens and stablecoin-focused L1 blockchains launching almost every week. But before we dive into that, let me first follow up on the liquidation event, this time from the perspective of stablecoins and market-neutral funds.

As Fiskantes mentioned earlier, these events aren’t new to crypto. Only the scale was. What’s changed since one of the first “events”, the Mt. Gox bankruptcy in 2014, is everything though. There were no perps, no stables, and barely any HFT (High-Frequency Trading) firms back then. I still remember Bitcoin trading at a 10% premium on Mt. Gox in the days leading up to the withdrawal halt. Fiat deposits and internal BTC transfers between Mt. Gox users still worked, even though fiat withdrawals had already been severely restricted. This created the potential for an interesting arbitrage, but one piece was missing: a secondary exchange where one could trade real BTC for Mt. Gox BTC. Within 48 hours, someone built one and called it, “uniquely”, Bitcoin Builder. It was rough, but it worked…, until Mt. Gox declared bankruptcy a few days later.

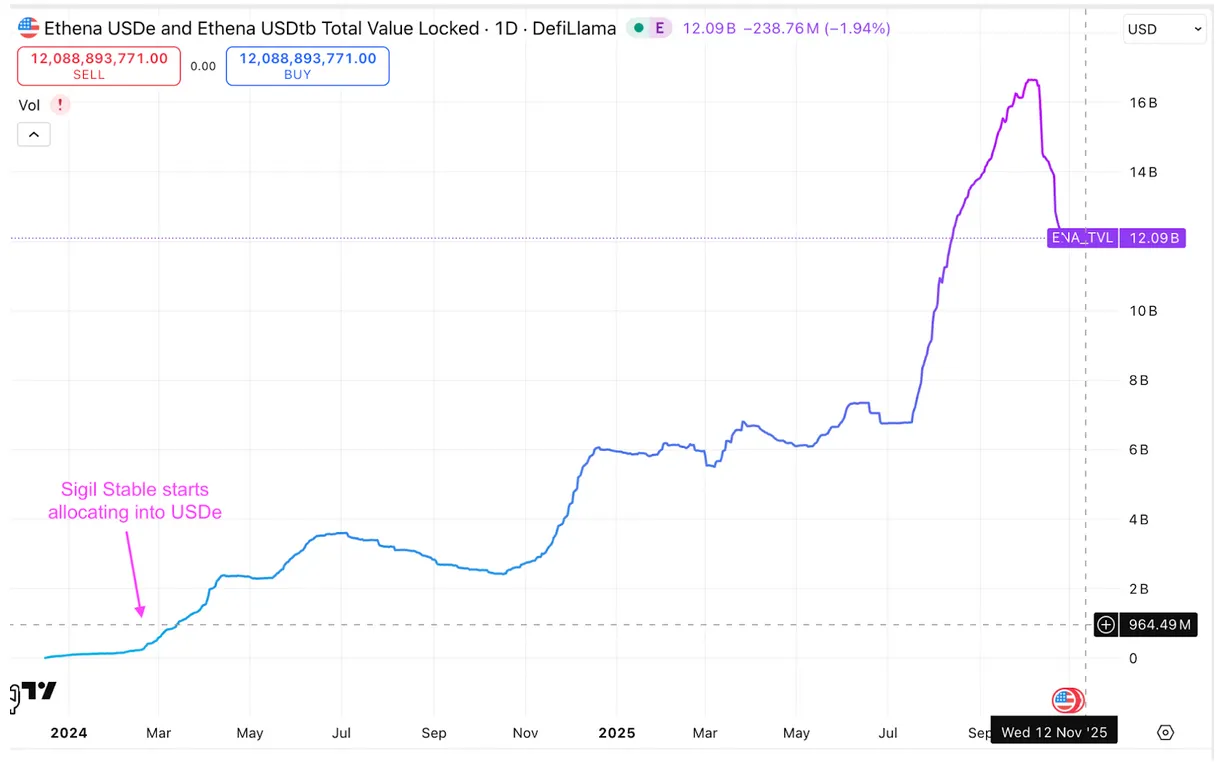

Now, back to the October 10th event. Never before had stablecoin supply been so high: $300 billion, a 100% increase since the FTX bankruptcy in November 2022. Another important difference was the new generation of stablecoins available as collateral on T1 exchanges, especially Ethena’s USDe on Binance. Let me expand on that, since Sigil Stable has been an early adopter of USDe since its launch in early 2024. Deploying USDe into various on-chain yield strategies contributed positively to our 35% net performance last year.

But USDe isn’t really a stablecoin. “Tokenized hedge fund” might be closer to the truth. Ethena runs a basis trade using ETH and BTC to back USDe. The tokenization idea of this trade isn’t new, but Ethena was the first to execute it flawlessly and scale it to billions. By early October, USDe’s supply had reached $15 billion. Ironically, the FTX implosion was what made structures like this possible. The market demanded off-exchange exposure with verifiable custody, and the infrastructure finally delivered: CEFFU for Binance, Copper ClearLoop for Bybit, OKX, and Deribit (disclaimer: Sigil is a Copper client). So even if an exchange “pulled an SBF” and turned user deposits into a VC fund or a fleet of Toyota Corollas (SBF’s “favorite” car), the worst-case loss for Ethena would be the unsettled PnL before the next margin cycle.

Ethena TVL, source: TradingView

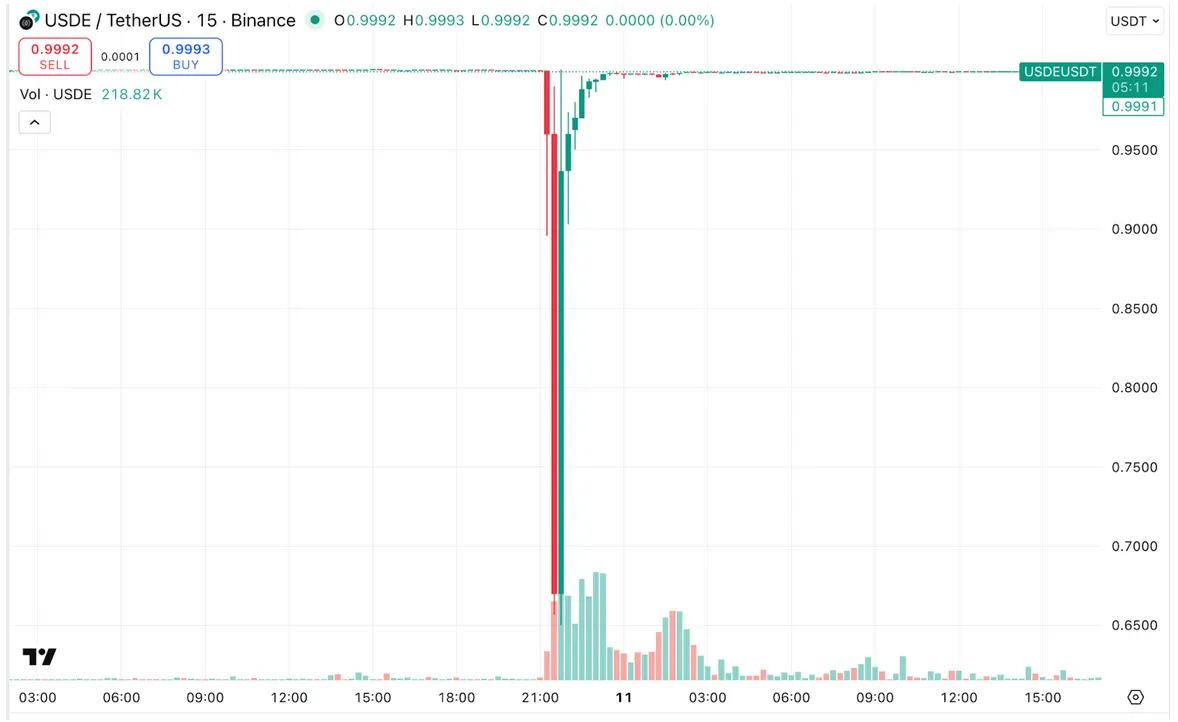

Binance listed USDe and allowed it as collateral for perps in September. Then came the infamous Trump tweet, followed by a $90 million USDe sell order. Within minutes, the token traded down to 0.65.

Was that a depeg? Not really. Ethena actually turned a profit for staked USDe holders. The founder summed it up nicely: “This is not USDe depegging; this is Binance depegging.” In other words, someone was selling dollars for 65 cents, and the counterparty was thrilled to buy them. Binance just happened to be in the middle.

USDE/USDT 15-minute chart, source: TradingView

Binance had made one serious design mistake though, it used its own USDe/USDT market rate as the oracle for USDe collateral. So even if you were directionally correct, say short BTC, you could still be liquidated if you used USDe as collateral and ran any meaningful leverage.

Sigil Stable and October 10

Let’s start with Ethena exposure. Sigil Stable had zero exposure to USDe as collateral on Binance futures. We had one hedge open on Binance during the event, and even if it had been collateralized with USDe, our leverage was below 1x, so we would have been fine.

We did, however, hold USDe exposure in DeFi, specifically on Aave (Plasma chain) as collateral with a borrow position in USDT. The position stayed healthy during the “depeg” since Aave had hardcoded the USDe oracle to USDT. If that hadn’t been the case, we wouldn’t have entered the position. Oracle pricing is the most critical factor when interacting with money markets in DeFi.

Hardcoding was clearly better than Binance’s setup, though not perfect either. In the very unlikely event that USDe actually depegs, DeFi money markets could end up with bad debt. And when that day comes, CZ will probably tweet: “This is not Binance depegging; this is USDe depegging.”

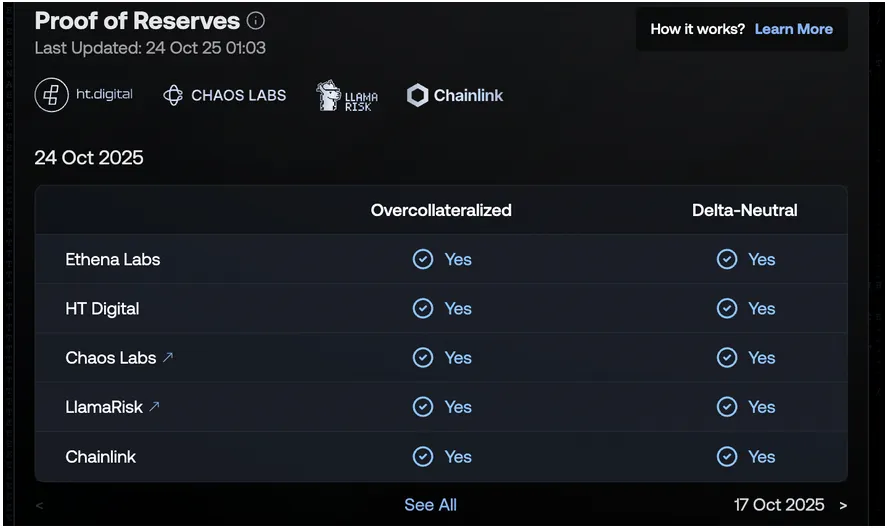

The space is maturing. Ethena launched its Proof of Reserves program in April with several independent attestors. Once it updates more frequently than weekly, it could become a core input for oracle design.

Ethena’s proof of reserves, source: Ethena transparency page

Other Strategies

12% of our portfolio is allocated to a leading HFT firm that no longer accepts new subscriptions. They thrived in the chaos, generating over 1% net return during the event.

Our hedged positions on perpetual futures venues remained healthy and were not auto-deleveraged.

All but one yield farming position were unaffected. The exception was the Lighter Liquidity Pool (LLP). Lighter, a Hyperliquid competitor, has recently gained traction, even surpassing Hyperliquid in volume. LLP’s design differs from Hyperliquid’s HLP, an interesting comparison we’ll save for another letter. LLP worked as intended but took a 5% drawdown as it absorbed liquidated long positions, unlike Hyperliquid, which ADL’d shorts. We’ve been early LLP allocators since March, and despite this drawdown, we remain significantly up on the position.

Sigil Stable closed the liquidation weekend without any loss. Good risk management and deep knowledge of the ins and outs of DeFi allow us to protect capital during periods of turbulence and consistently generate yields for our investors.

USD.ai

Moving on, in the previous letter, we hinted at a high-quality private liquidity deal. It came to fruition in Q3. Since the project announced it publicly, let’s double click on it.

USDai is pitched as a fully-backed synthetic dollar that derives its backing from AI infrastructure and tokenised compute assets rather than boring short-term T-bills (though those still serve as fallback reserves). The protocol structures users into three roles: depositors mint USDai and stake into sUSDai (yield-token), borrowers (AI operators) draw liquidity against hardware, and curators bear first-loss risk to make the whole stack investable.

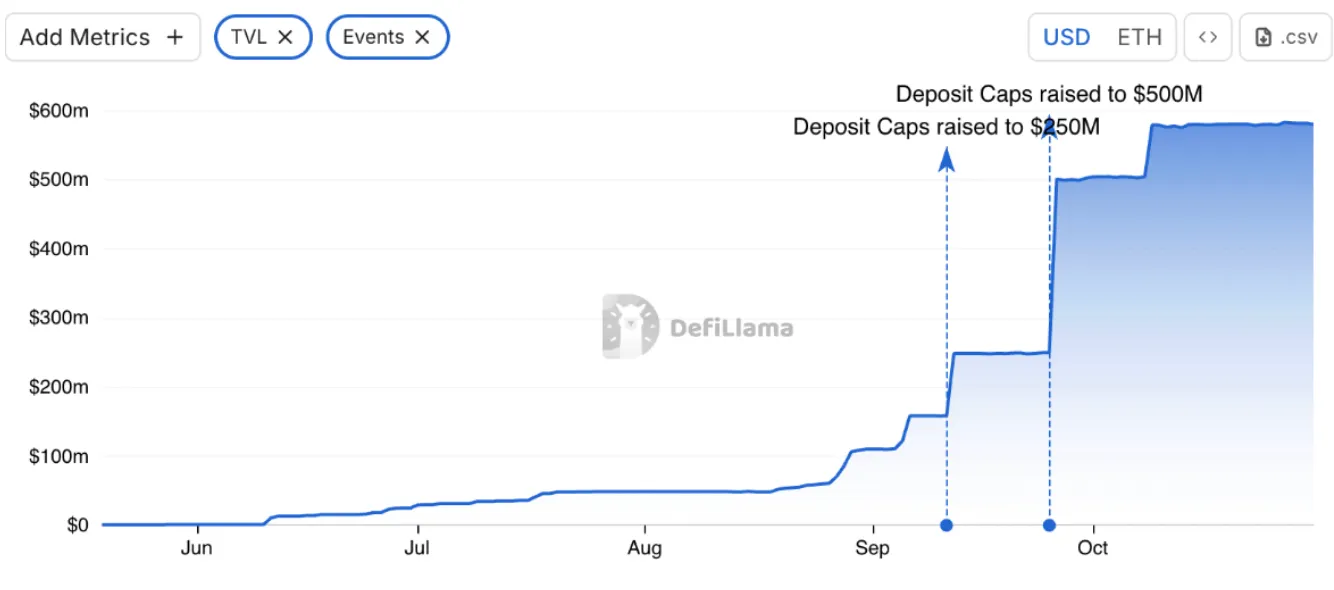

Sigil Stable and Sigil Core both participated in USDai’s private liquidity deal when TVL was below $30 million. Since then, USDai opened to the public and has seen tremendous success in attracting liquidity. Supply now sits at $580 million, and the only reason it isn’t above $1 billion is the hard cap.

USDai TVL, source: Defillama

Each time the team increased the cap limit, it was filled within minutes — sometimes seconds. Earlier we discussed Ethena’s USDe depeg. Well, USDai had one too. You can probably guess the direction, but what might surprise you is that it traded 600 basis points above $1 in early October. There’s no room for cigars yet. Yes, the demand was massive, but the upside depeg wouldn’t have happened without the hard cap throttling supply. A full cap lift is planned once the initial bootstrapping phase concludes.

USDai is planning a TGE (token generation event) once it reaches $20 million in revenue or after six months of operations, whichever comes first. Both Sigil cells will receive their token allocations after the event, subject to a lockup as part of the liquidity deal. If our bullish view holds, it’s likely going to be great news for both Sigil Core and Sigil Stable.

Plasma launch

Since this letter is already too long, I’ll spare you the long definitions. Plasma is an L1 for stablecoins.

Following up on our Q2 letter, our on-chain bot secured a small allocation in the Plasma ICO even after the cap was hit. The bot executed a deposit transaction immediately after a slot became available when a user withdrew their allocation. Thanks to this, we were able to secure a higher allocation later on by slightly overbidding, assuming not all eligible users would allocate the maximum during the ICO. The gambit worked, although not to the extent we had hoped, since less than 0.2% was available for grabs pro rata. No surprise there — Plasma was already trading at 10x the ICO price on premarkets at that time.

Let’s double-click on XPL pre-markets, since that’s where another bit of drama unfolded. Perpetual futures rely on index prices: reference values used to anchor contracts to the real spot market. In normal conditions, the spot is the dog, and the perp is its tail. But in pre-markets, there’s no spot, just the tail wagging itself. It’s a perfect setup for opportunists, and in Plasma’s case, they showed up.

XLPUSD 1-minute chart, source: Hyperliquid

The “attacker” claimed a fat-finger error, executing much larger market long orders than intended. The result: XPL tripled in price within five minutes, leaving short sellers no time to top up collateral before being liquidated. Since ADL was triggered, the attacker was forced to exit his longs perfectly, pocketing tens of millions. He’s either the world’s luckiest incompetent trader or one of the sharpest executors of an economic exploit in recent memory.

Moving on, the last XPL incentives before its TGE in late September were distributed to syrupUSDT depositors on Midas. The $200 million cap was hit within minutes, even before the UI went live. Our trading desk anticipated the move through on-chain analysis and successfully deployed capital into the vault. Having deep knowledge of interacting directly with smart contracts and leveraging on-chain bots in certain instances has proven to be a significant edge for us on multiple occasions. We are constantly refining and improving these capabilities to accrue steady yield generated for our investors.

Q4 Outlook

Sigil Stable remains well positioned to capture opportunities arising from the evolving stablecoin and infra landscape. We are active on several perpetual markets expected to launch native tokens later this year or early next, where early liquidity and asymmetric setups have potential to offer strong risk-adjusted returns. Alongside these, we hold allocations in multiple private liquidity deals that are still under wraps but share the same theme of strong expected yield. It was a busy summer in the stablecoin world, and the momentum has clearly carried into Q4.

Thank you for your ongoing trust in the Sigil fund.

— Joe, Investment Partner heading Sigil Stable trading.

If you’d like to discuss your investment, please don’t hesitate to reach out to us at info@sigilfund.com.