Dear Investors,

year 2022 was probably the most turbulent year in the history of crypto markets. Many market players disintegrated, including some of the largest funds, exchanges and lending desks. The unexpected implosion of key players combined with a negative macroeconomic situation led to a series of market-wide price crashes, leaving many investors scrambling for exit.

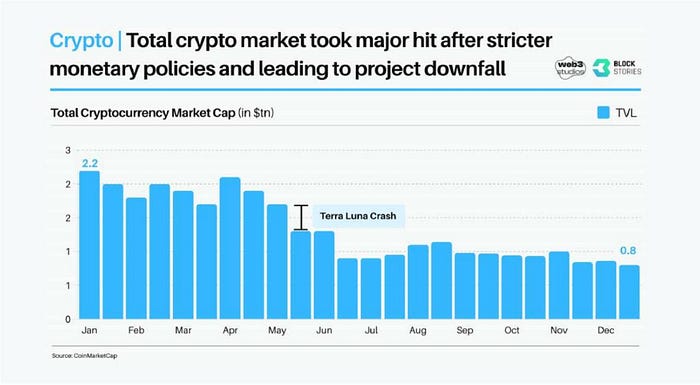

The scale of negative events was unprecedented and once again proved the cyclical nature of crypto markets. The total crypto market decline in 2022 was significant (-63,64%) but as many times before, crypto survived and came out of the storm stronger. Developers continue building innovations with revolutionary potential, blockchains keep producing blocks, DeFi continues providing permissionless financial infrastructure, replacing some of the centralized players who were wiped out. One of the biggest positive news of last year was the successful Ethereum Merge which went so smoothly it surprised even the biggest optimists among us.

In case you need to refresh all the major stories you can find them in our previous letters to investors: [Q1, Q2, Q3].

The fourth quarter continued the trend with setbacks but also positive changes, which we will elaborate on in this letter.

In the Q4 of 2022, Sigil Core recorded -22.74% vs EUR, -0.42% vs BTC. Over the course of the entire year 2022, the performance of Sigil Core was -60.84% vs EUR, +3.65% vs BTC.

Sigil Stable saw a decline in yield due to market conditions. In Q4 we booked a loss on FTX via an indirect investment to a third party (market-neutral algorithmic strategy).

Sigil Stable recorded a performance of -12.62% vs EUR, -4.38% vs USD in Q4 2022 and finished the year 2022 with performance +2.26% vs EUR, -3.56% vs USD.

Sigil Core Net Performance vs EUR Q4 in 2022

Sigil Stable Net Performance vs EUR Q4 in 2022

Macro situation

During the fourth quarter, the Federal Reserve maintained its previously announced policy and increased interest rates by an additional half a percentage point.

From a macroeconomic perspective, a more significant development in this period was the shift in policy at the Bank of Japan which adjusted its loose monetary policy. The Bank of Japan caught the markets by surprise as it had decided to allow the 10-year bond yield to move by 50 basis points in either direction around its 0% target, which was a wider range than the previous limit of 25 basis points. That happened probably due to the weakening of the yen against the dollar, and in view of the previous policy, the alternative form of action was preferred to rate hikes.

Overall, markets appear to believe that central banks will continue to increase interest rates until inflation is under control. Thre are indications of one last FED hike to be expected during 2023. However, if a recession were to occur, the printing of additional money by central banks could potentially help to stimulate the markets. This in turn could help the markets bounce back from the recession. It’s quite likely the elites will go back to looser financial conditions as soon as the inflation allows them — due to notoriously well- known reasons like excessive debt across both public and private sectors.

FTX crash

Starting in early November 2022 and continuing up until this day, there has been widespread media coverage of the financial problems, fraud, and the ultimate insolvency of FTX, the at the time second largest cryptocurrency exchange by volume. Sam Bankman-Fried, the founder and former CEO of FTX also known as SBF, faces multiple charges, including conspiracy, securities fraud and money laundering. If convicted, he could face up to 115 years in prison.

There have been many wrongdoings and questionable acts which have been extensively covered by all mainstream media. To highlight the major ones, SBF with FTX and Alameda leadership:

- contributed over $40 million to the Democratic Party in the 2022 election cycle and maintained close relationship with policy makers, in order to posture as legitimate and highly regulated player

- lobbied for such regulation of DeFi that would potentially enable FTX and other incumbents to capture the market and build a regulatory moat

- commingled FTX customers’ funds with own assets and lent them to Alameda (and potentially used them elsewhere too)

- used exchange’s FTT token as collateral while overblowing its valuation and ignoring its liquidity

- acquired multiple 8 digit properties while posing as a “frugal effective altruist” for PR

- was actively spreading false information publicly to keep users from withdrawing funds from FTX

- as a result, a hole of more than $8 billion was created between FTX customer assets and liabilities, which led to bankruptcy of FTX exchange (both .com and .us) and the Alameda trading firm.

You can find the full story of the FTX collapse here.

Markets were already shaken by previous meltdowns (3AC, Luna and several lending desks) but the sudden bankruptcy of FTX came even more unexpected. Cryptoassets that were supported by FTX and Alameda fell the most. Solana (SOL) lost 97% from its ATH value and dragged down big funds which had substantial exposure to it. Sigil fund managed to avoid direct losses by 1) acting quickly to withdraw and protect the capital and 2) by shorting SOL for extra profit. You can read more about it in our previous letter to investors.

Binance FUD (Fear, Uncertainty and Doubt)

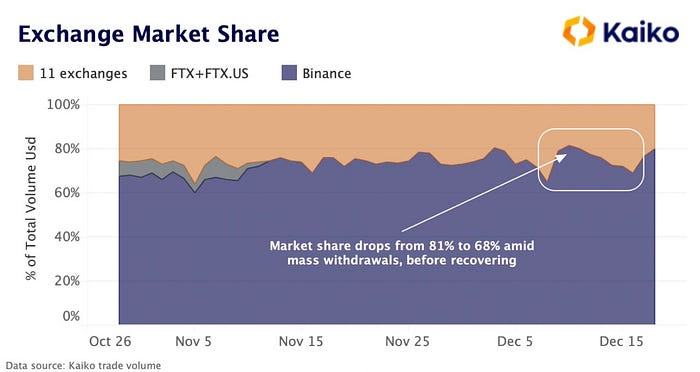

CEO of Binance - Changpeng Zhao expressed interest in trying to bail out FTX. During due diligence, Binance found major problems which made them withdraw from the deal. In their own words “The issues are beyond our control or ability to help”.

The distrust in the markets in the month following the FTX crash caused also a bank-run on Binance itself. The exchange experienced net outflows of around $6 billion over 72 hours. With a large number of cash outflows, they temporarily suspended USDC withdrawals. In November, Binance had a market share of nearly 75% of all global crypto spot trading volume. It is estimated that Binance generated up to $6.4 billion in revenue in 2022, which should allow them to weather any downturns without significant difficulty.

We at Sigil, however, take no chances and hold the vast majority of our assets on-chain, away from exchanges or any other third party custodians who could put our assets at risk.

DCG FUD

The negative market conditions also affected Digital Currency Group (DCG), forcing its CEO, Barry Silbert, to announce that one of their group companies owes $2 billion to its subsidiaries and outside creditors.

DCG is a conglomerate consisting of notable companies in the industry, including Genesis (the largest crypto prime broker and a lending desk) and Grayscale (an asset management firm), and was once valued at $10 billion, with billions in assets under management.

Most eyes are set on Grayscale, the “cash cow” of DCG, which operates the most significant institutional investment vehicle for all cryptocurrencies — the Grayscale Bitcoin Trust (GBTC). Due to the dampening of confidence in its parent company, GBTC credibility was called into question. This sent GBTC shares plummeting down and trading at over 45% discount to the value of Bitcoins held in the trust.

Remember me for faster sign in

At the time of this article’s publication, Genesis Global Capital, LLC filed for bankruptcy under Chapter 11. The bankruptcy of the lending desk put a bad light on the whole DCG group. DCG is working on resolving the heated situation with creditors, particularly with Gemini - a crypto exchange that operates a lending program Gemini Earn, which was promising an 8% yield and was forced to suspend withdrawals due to allegedly Genesis owing them $1.675 billion.

Common factor

All the events described have one common aspect: failure of the centralized custodian trusted third parties. Precisely the thing crypto was supposed to replace. While holding your crypto-assets with custodians is often simple and user-friendly, it will always carry more risk, especially when the custodians get greedy and start to use user funds in risky endeavors, while users have no visibility where their assets are really stored. This puts centralized third parties in stark contrast with decentralized crypto protocols where data is freely available on chain 24/7.

We do not naively foresee that centralized custodians will disappear for good. They will always offer attractive trade-offs when it comes to UX, simplicity and efficiency. But we definitely expect better auditing practices from key players such as providing public proof-of-reserves and proof-of-liabilities. There are now approximately $200 billion in cryptocurrency assets held on exchanges that can be fully accounted for and tracked. No such audit will ever replace the elegant, open and transparent nature of public blockchains where any user is able to independently verify what exactly is happening with all the assets in real time.

We also expect regulators to finally stop going after non custodial and transparent DeFi projects and start regulating what they should be regulating — big centralized entities who control billions of (mostly) retail owned assets. Practice shows time and time again that the greedy human nature is the problem in our industry, not the transparent technology of crypto protocols.

New L1s

In October, new contestants entered the highly competitive L1 market: Aptos and Sui, which are spinoffs from the discontinued Libra project by Facebook. These blockchain raised private rounds for nosebleed valuations and created a lot of hype in the process. Sigil is not positioned in these new L1s. While markets often flock to “new shiny thing” projects and chase hype, we understand that building a successful and sustainable blockchain ecosystem takes a lot of time and effort.

We won’t consider investing in any of the new flavor L1s until we see clear signs of sustainable traction. Traction in terms of development activity, innovative products and customer adoption — not the financial engineering of VC investors (which, if anything, might warrant tactical short positions at the peak of absurd valuations on L1s that have nothing real on them).

Ethereum

We remain well positioned and bullish on ETH and its ecosystem. EVM (Ethereum Virtual Machine) has by far the largest developer community and user traction among blockchains. Ethereum’s roadmap can be considered the most elaborated as compared to its competitors. According to the Crypto Theses for 2023 report by data analytics and research firm Messari, ETH holds a 70%+ market share in what they call “neutral” L1 space (netting out Binance’s own BNB token), claiming there’s about $155 billion of ETH and $57 billion of “other L1'’ assets.

The Merge is another reason why we are currently positioned heavily in ETH. This change reduced the ETH issuance rate which used to be approximately 4.09% (4.93M ETH) per year to effectively zero inflation. You can track the ETH issuance rate and other interesting data points at ultra sound money which we highly encourage you to check out (warning: it will make you super bullish). The inflation rate since the merge oscillates around zero depending on usage of the Ethereum network. As a reminder the balance in ETH inflation is achieved by two forces:

- new ETH is minted and awarded to stakers for supporting the network

- existing ETH is burned in form of gas fees when the Ethereum network is used

To put this into perspective: So far one of the major drivers of crypto cycles are Bitcoin halvings (50% reduction of newly mined BTC supply every 4 years). Last halving reduced the new yearly issuance rate from 3.65% to 1.80%. The Ethereum Merge single handedly delivered a change that Bitcoin halvings will have gradually produced over the next decades.

We believe ETH supply reduction will have a material impact on the upcoming bull cycle.

On top of that, the transition to PoS (Proof-of-Stake) brought by the Merge eliminated the need for energy-intensive mining equipment and replaced it with a more economical staking mechanism. The new Green Ethereum that is environmentally friendly has been warmly welcomed by all global media.

In the new PoS, validators instead of miners are in charge. To become a validator of the network, operators must stake 32 ETH, roughly $50,000 at the time of writing. The downside is when a validators stake 32 ETH, it ties up their capital incurring opportunity costs.

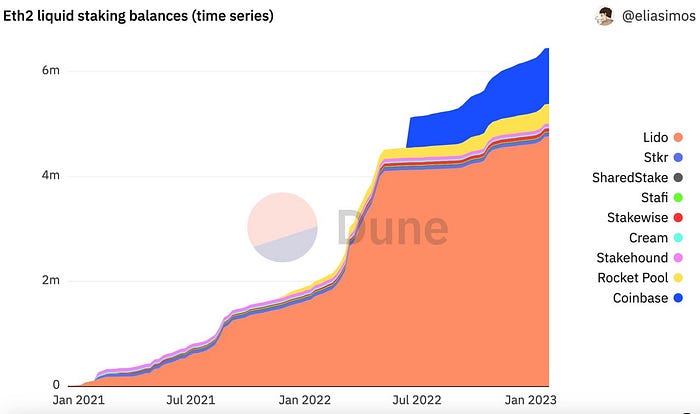

Liquid Staking Derivatives

This is where liquid staking derivatives (enabled by projects such Lido or Rocket Pool or exchanges like Coinbase) step in.

First, they lower the barriers to entry for staking by allowing to stake even a fraction of ETH to earn a return around 5% p.a. These protocols also deal with technical challenges associated with the running of the nodes and ensure their 24/7 operation. In order to tap into this locked (staked) capital, a derivative token is created, serving as a fully liquid claim to its underlying staked ETH and rewards accruing from its staking. Because it’s fully liquid, this derivative token can then be transacted with, used as collateral and for other financial operations, especially in DeFi. Hence the term Liquid Staking Derivatives (LSD).

The LSD trend started to gain market attention in Q4 2022 and continues into Q1 2023. The upcoming Ethereum upgrade known as “Shanghai fork” in March, which will unlock staked ETH for the first time since 2020, is an opportunity for growth in the liquid staking space where Lido is the clear leader. Sigil Core booked profits from its Lido position several times including Q4 2022:

Layer 2

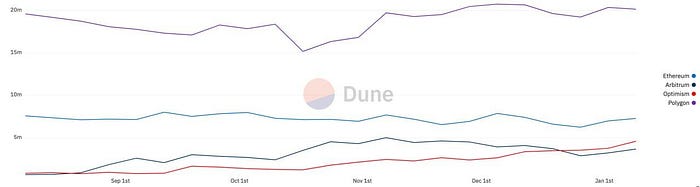

Additionally, Layer 2 solutions have significantly aided in ETH’s scaling efforts. Transactions on Layer 2 surpassed those on the main chain (Layer 1) already in September, with Optimism, Arbitrum and Polygon leading the way. At the same time, more technically advanced Zero Knowledge rollups (StarkNet and ZkSync) carry even more promise but will take longer time to market adoption. We are eager to see some early adoption of ZKs in 2023 but we don’t expect them to gain major traction.

What can drive the next bull cycle?

While we are not in the business of timing markets, our opinion is that crypto prices already reached their bottoms during last year’s meltdown. Unless we see more black swan events, we can expect markets to start recovering. There is also a good chance that the macro economic situation could improve, and crypto as a 24/7 risk-on market is usually the first canary in the coal mine for a new macro sentiment.

These could be some potential drivers of crypto adoption in the next bull cycle:

1. Web 3 Gaming: We may see first crypto native games that are fun to play and have a sustainable ecosystem and tokenomics. Two examples we feel particularly optimistic about are Aurory and Parallel. We have referred to Aurory in one of our previous articles. What’s new since then is that you can already play the game, participate in leaderboards, win AURY tokens and much more. If you’d like to see a short game preview, check out this video.

Parallel started with its NFT drops as a collectible card game and captured a huge fanbase with its spectacular artwork. It will open a testing period this February. However ambitions of Parallel team are much bigger — to become a web3 gaming and media franchise. You can check out this short video to find out more.

2. In previous cycles BTC was leading the bull markets. This time, however (as we already mentioned) it could just be ETH and the Ethereum ecosystem driving the markets upwards and capturing the attention of institutional investors, with its crypto native staking yield and LSDs.

3. Alternatively, the next crypto cycle could be kicked off by the BTC halving (like the previous ones). Halving is expected to occur in March/April 2024. To refresh one’s memory, prior to the last halving event, the value of BTC experienced a significant surge, growing from roughly $7,000 in the beginning of 2020 to over $10,000 by April of that year. After the halving, the price continued to rise reaching an all-time high of over $64,000 in April 2021.

4. While the USA is still a hub of free technical innovation in many areas, its unclear (and sometimes even hostile) regulatory position towards crypto could leave the opening for Asia. This region is well-positioned to be at the forefront of the next wave of innovation and investment frenzy. Factors making us optimistic about Asian crypto markets include:

- large, growing and young population of retail investors and consumers

- markets for fundraising and capital formation which are not well served by traditional financial infrastructure

- growing acceptance and support of crypto from governments and institutions

- access to relatively cheap engineer workforce

- consumers being educated and used to financial superapps and other digital innovations

5. Pragmatically speaking it could also be just the macro and general cycle that will kick start the growth in crypto prices again. The above mentioned crypto catalysts will just be an additional oil into the fire. It is broadly expected we will see one last FED hike in 2023 and then natural return to bull markets in risk-on assets.

Seizing the moment

At Sigil, we are steadfast believers in the transformative power of blockchains and crypto and its ability to disrupt multiple industries. In Q4 Sigil Core started redeploying its stablecoin holdings back into high-potential opportunities in order to secure the maximum returns and to capitalize on the opportunity at hand before the next market cycle starts.

As it is impossible to perfectly time the exact bottom, we advocate for a smart strategy of buying assets when they are at perceived lows, particularly for those with a long-term investment mindset. It takes bold decision-making and courage to make moves when others are hesitant and to have the ability to navigate market downturns. This approach in current market conditions presents a unique opportunity for investors as crypto markets have the potential to offer outsized returns to those who can stomach the volatility.

No winter lasts forever and we have been in a bear market since Q4 2021 market tops. We are cautiously optimistic for 2023 and believe it is a strong idea to consider depositing to Sigil Core fund to position yourself for the coming bull market. We have weathered the storm much better than others and have been overperforming the benchmark of global crypto funds over the past 3 years. We are looking forward to the future periods and thank you for your ongoing trust in Sigil fund.