Table of contents:

In Q4 2025 Sigil Core returned:

- -22.28% net of fees against EUR

- -22.31% net of fees against USD

…and beat the BTC benchmark by 1.2% net of fees:

Over the full year 2025, Sigil Core delivered the following net returns:

- -12.89% net of fees in EUR

- -1.25% net of fees in USD

- +5.52% net of fees in BTC

Sigil Core

2025 proved a difficult year for crypto. Despite regulatory tailwinds, the market failed to generate meaningful returns. While the Trump administration ended the previous “war on crypto,” crypto swapped the regulatory hostility for fresh macroeconomic and geopolitical uncertainty. Gold outperformed Bitcoin as a “geopolitical hedge,” and AI stocks overtook crypto as the premier “tech risk-on asset.” Sigil Core finished the year roughly flat, notably outperforming the BTC benchmark.

Following the unprecedented liquidation event on 10 October (referred to as “10/10 event” in crypto circles), market participants were forced to de-risk and reposition. While the “who” and “how much” remain opaque, some major players took significant haircuts and were forced to sell excess exposure. We have yet to see any bodies float to the surface, and with the passage of time, a total blow-up of a major player seems increasingly unlikely. However, a caveat remains: some actors are skilled at covering their tracks, and we may not yet know the full extent of the damage.

The troubled fate of DATs

In our Q2 letter, we covered the rise of Digital Asset Treasuries (DATs). At that time, they were a “hot trend”; the “Saylor Strategy” was trading at an mNAV of 1.92 (a 92% premium to its BTC treasury). As we predicted, this mania was short-lived. At the time of writing, the self-reported Strategy mNAV has compressed to slightly above 1. It is entirely possible we will see it trading below treasury value in the near future.

Most other DATs are already trading at deep discounts to their underlying treasuries. While these stocks may appear to be an attractive way to acquire crypto assets at a discount, important caveats remain. Management maintains full discretion over these treasuries; while some may choose to divest assets to fund share buybacks, others are opting to diversify or acquire productive businesses to become more active players. We expect some DATs to shutter as shares continue to trade at deep discounts and shareholders (or activist investors) increase pressure. Much like the aftermath of the 10/10 event, the unwinding of the DAT trade (primarily the smaller, tier 2 companies) will likely act as a short-to-midterm drag on market performance. We do not expect sentiment to shift without a meaningful catalyst, though at some point, these discounts may offer asymmetric opportunities for savvy market participants.

Within the DAT sector, Sigil Core is invested in Forward Industries (FWDI). It currently trades at a discount to its holdings and we are betting on the world-class team to drive added value to their holdings. We expect the stock to act as a high-beta exposure to SOL, and when the market sentiment shifts we are betting on it to trade close to its mNAV. In the meantime, the SOL in the treasury will earn substantial yield. In general we believe high yielding utility assets such as SOL or HYPE are better suited for DAT mandates than more passive assets such as BTC.

Lighter TGE

The quarter’s final major milestone was the December 30th TGE of Lighter (LIT). As the second-largest perpetual DEX by volume, Lighter is the primary challenger to Hyperliquid. We view Lighter as a high-potential alternative. Expecting both to capture significant market share of the growing perpetuals pie as on-chain perps go mainstream, we have added LIT to our portfolio while keeping HYPE as a core conviction holding.

On de-risking

You are invested in Sigil Core because you believe in the long-term adoption of crypto. Our primary goal is to fulfill that mandate by identifying asymmetric upside. However, we also recognize when the risk-reward ratio shifts unfavorably. When we see a lack of quality opportunities or emerging structural risks, we believe the most responsible action is to take a step back.

Our standard cash allocation usually fluctuates between 10% and 30%. In exceptional circumstances, we move outside those bounds — in 2023 we were fully deployed and our max long maximized gains for investors. Conversely, as the risk reward started looking unfavourable in Q4 we de-risked 40% of the portfolio. This is also the first time in our fund’s history where we have 0 BTC and 0 ETH exposure. We believe this defensive positioning is necessary to navigate the current environment while remaining ready to redeploy when conditions improve.

Since many of you have inquired about this shift, here is the full reasoning behind our decision to de-risk:

1. Macroeconomic and Geopolitical Outlook: Our short-to-midterm outlook remains cautious. We are witnessing a volatile transition from the US-led unipolar economic system — which has dominated since the fall of the Soviet Union — toward what will likely become a multipolar world order. This transition is marked by increasing armed conflicts, geopolitical tensions, and fiat currency debasement. Historically, such environments are unfavorable for most “risk-on” assets.

2. The Safe-Haven Paradox: While we believe Bitcoin and digital assets should serve as a hedge against such uncertainty, recent data suggests otherwise. Over the last year, Bitcoin has largely decoupled from Gold and has struggled to perform as a traditional safe-haven asset. Ironically, this underperformance coincides with the US establishment finally embracing crypto. As more US institutions adopt Bitcoin, its “credible neutrality” may be coming into question for the rest of the world. In the wake of the 2024–2025 geopolitical shifts and the freezing of foreign sovereign assets (like what happened to Russia in 2022), non-Western leaders may increasingly view a US-integrated Bitcoin not as a neutral alternative, but as another extension of the Western financial system.

We believe this view is overblown and in reality Bitcoin remains neutral and decentralized but we understand such a narrative can become a consideration for major capital allocators.

3. The Maturity of the Crypto Hype Cycle: We have always categorized the broader crypto market outside of Bitcoin as an “innovative, techno-optimistic” asset class rather than a “flight to safety” play. It is a transformative technology redefining how we store and transfer value — the backbone of what we call the “Fintech 2.0” stack.

Since 2018, we have witnessed crypto’s transition from a niche, experimental landscape dominated by scrappy founders and libertarian idealists to a multi-trillion-dollar industry inhabited by corporations, financial institutions, and sovereign governments. This evolution was inevitable; it has become clear that crypto — despite its flaws — offers a superior technical foundation for 21st-century finance compared to legacy banking. While we anticipated this shift earlier than most, it is no longer a contrarian view. It is now the consensus, and as a result, the easy asymmetric upside has diminished.

The risk-reward profile today is fundamentally different than in 2018. Back then, the risk of “crypto going to zero” was a legitimate possibility, and we were compensated for that risk with exponential returns. Today, while individual assets may still fail, crypto’s existence as a permanent industry is virtually undisputed. However, as the sector matures, its growth will naturally become more muted and subject to the same economic gravity as other established industries. At a $4 trillion total market cap, the industry can no longer trade on narrative and expectations alone. It must now deliver tangible utility against which the valuations need to be compared.

The cracks in market structure

Today, crypto enjoys regulatory and adoption tailwinds from the US government, major institutions, and ETFs. However, it also faces significant structural headwinds that weigh heavily on the market. Most notably:

1. Persistent Supply Overhang: The market is currently struggling with a massive supply overhang. Vested tokens from a plethora of projects are constantly hitting the secondary market, as early investors with a low-cost basis seek to unwind or hedge their exposure. This systematic selling pressure has found it difficult to meet consistent, sustainable demand. Simply put, there are not enough systemic buyers in the secondary market to absorb the sheer volume of supply being unlocked. In many instances, the “fully diluted valuations” (FDV) at which these tokens are launched are unappealing to sophisticated investors, leaving the market to rely on short-lived momentum from retail traders that quickly evaporates.

2. Incentive Misalignment: The “rule of terror” from the previous administration’s SEC forced a generation of crypto projects to strip their tokens of protective rights or value-capture mechanisms to avoid being classified as securities. This has left the market riddled with “pseudo-equity” assets — instruments that provide volatility for short-term traders but offer little to no long-term utility for serious capital allocators.

In traditional US equity markets, an investor’s primary job is to analyze business fundamentals and macro trends; legal rights and shareholder protections are already baked into the institutional framework. In contrast, a significant portion of our due diligence at Sigil consists of deconstructing tokenomics to see if value actually accrues to the holder. Too often, we find world-class teams building great products with non-existent value-capture mechanisms. During the industry’s experimental phase, investors were willing to overlook these flaws in exchange for massive upside, operating on the philosophy:

“Build it and capture market share first; figure out the value capture later.”

Today, investors no longer tolerate this view. Tokens backed by little more than “trust me” guarantees have become a drag on the market’s credibility. While we still navigate these assets for tactical trades, we do so with short validation horizons and a high bar for entry.

Gartner provides a helpful framework for understanding the current state of crypto.

The points above might seem pessimistic, but they are a sign of the standard “hangover” that follows every massive hype cycle. The “party” of the last few years has ended, and we are now dealing with the cleanup.

Taking the long view, we believe this self-correction is vital. The industry is trimming the fat and flushing out the bad actors and misaligned incentives of the previous era. As we move past this trough, we expect to enter the “Slope of Enlightenment” — a phase defined by sustainable growth and the emergence of crypto as a mature, productive technology and asset class. Projects such as Hyperliquid who have a strong product market fit (and revenues) who treat their token holders like true stakeholders are finally seeing a “quality premium” in their valuations.

The Path Forward

Since 2020, we have witnessed a “Cambrian explosion” of projects across L1s, L2s, DeFi, infrastructure, gaming, and memecoins. This proliferation is inevitably followed by consolidation. We expect market leaders with established moats and network effects to cement their dominance — either by acquiring or displacing their competitors. While a few successful latecomers will emerge, they will likely need to create entirely new markets or operate at the idiosyncratic intersection of crypto and other emerging fields.

The next phase of crypto adoption will likely rhyme with the post-dot-com era. Just as the “internet” ceased to be a single category and bifurcated into e-commerce, social media, and SaaS, crypto will stop being viewed as a monolithic asset class. Over the next decade, we expect it to fragment: some segments will merge with traditional capital markets as institutions integrate the technology, while others will become the invisible backbone of the digital economy. Much like the FAANG companies that outperformed the broader market for two decades, we believe a few “big winners” will emerge from this consolidation to provide outsized returns for patient, high-conviction investors.

Our mission during this transition is to identify the “FAANG of crypto”. We are focusing on backing the next cohort of founders who are leveraging a mature tech stack to build novel, indispensable products. While some high-quality projects are already trading at deeply suppressed valuations, others remain overpriced with significant supply unlocks looming on the horizon. One of our goals for this year is to find these deep-value opportunities. From an investor point of view we simply want to “own winners who will keep winning” and “keep finding undervalued projects with a strong potential”.

Trends we are following in 2026 and beyond

1. The Institutional Convergence (Fintech 2.0): Financial markets are moving on-chain at an accelerating pace. We are seeing a convergence between DeFi and TradFi as a broad spectrum of assets — including stocks, commodities, private credit, and real estate — becomes tokenized. We believe this represents the birth of “Fintech 2.0.” While the first era of fintech was primarily about wrapping traditional payments and brokerage in a modern app, blockchains expand the design space dramatically.

We are actively deploying capital into this vertical. One of our high-conviction positions is Canton, a blockchain network led by a global consortium of financial institutions. Canton provides the privacy and regulatory-compliant environment required for banks to move from pilots to production. While many institutions are experimenting with public blockchains like Ethereum and Solana, Canton has emerged as the premier choice for conservative players who require enterprise-grade confidentiality and granular control.

2. Prediction Markets as Information Engines: Prediction markets have hit “escape velocity.” Since our investment in 2023, Polymarket evolved from a niche betting app into a household name in politics and journalism. However, this is only the beginning. We believe the true potential lies in their transition from retail entertainment into vital tools for information discovery. In a world of fragmented media and “fake news,” prediction markets can provide a real-time, money-backed signal in the noise of fragmented media and biased polls.

3. The Privacy Pivot: On-chain privacy is moving from a “cypherpunk niche” to a necessary feature. We are witnessing a dual push for private solutions. On the “anti-system” side, individuals are seeking wealth protection against increasing socialist “wealth redistribution” rhetoric in western politics.

On the “pro-system” side, institutional players simply cannot operate on transparent public ledgers where their strategies and positions are visible to every competitor. We believe the next phase of the cycle will reward protocols that offer “programmable privacy” — the ability to remain private by default while maintaining the hooks necessary for regulatory compliance.

Those who don’t study history are destined to repeat it, those who do are already thinking about how to best protect their capital and hedge against the “warmth of collectivism”.

4. Post Quantum Cryptography: Post-quantum cryptography (PQC) is set to become a dominant theme in 2026. Despite the ongoing hype, quantum computers are not yet viable for any practical commercial use. However, within a 3-to-10-year horizon, they may pose a credible threat to the legacy cryptography that currently secures almost all digital value. Fortunately, we already have “quantum-resistant” cryptography that can mitigate this risk. For traditional financial systems and agile blockchains, upgrading to these new standards is a relatively straightforward technical migration.

Bitcoin, however, remains a notable exception. Due to its decentralized nature, design philosophy and culture that intentionally makes updates difficult, Bitcoin will require significant global coordination and public discourse to address this threat. Transitioning the network to a post-quantum standard will likely trigger intense debate within the community. While we believe the problem is solvable, it will not happen without controversy or political friction. We will cover this topic in much greater depth in future writings.

In conclusion

Thanks to our prudent de-risking in Q4, we enter 2026 in a position of strength. We are well-capitalized and ready to selectively accumulate high-conviction assets at attractive valuations over the coming months. Simultaneously, should the market find a catalyst and reprice violently to the upside, our majority position in Sigil Core ensures we remain well-positioned to capture that momentum.

I’m sure you want to know when the prices will recover. The truth is, we cannot predict how long this “hangover” phase will last or what the next Fed chair does, etc. We can only position as best as we can for all possible outcomes.

We believe in having strong views, loosely held. In a market as dynamic as crypto, rigidity is a liability. We will continue to adapt our exposure as new data emerges, but our fundamental goal remains the same: navigating the volatility of this industry to deliver the best long-term exposure to the secular trend of global crypto adoption.

Thanks for your ongoing trust in the Sigil Core fund.

— Fiskantes and the Sigil team

Sigil Stable

Sigil Stable Q4 2025 update

In Q4, Sigil Stable delivered a -0.37% net yield after fees for our investors, with a Sharpe ratio of -0.5.

Over the full year 2025, Sigil Stable delivered the following net returns:

- +11.29% net of fees in USD

- +18.92% net of fees in BTC

with a Sharpe ratio of 2.86.

Market Landscape

The dominant theme in Q4, which took a bite out of a lot of market-neutral and delta-hedged funds, was the October 10 liquidation event. We went in-depth on Ethena’s USDe in our previous quarterly letter. Calling it a stablecoin is convenient, but “tokenized hedge fund” is closer to the truth, especially when the market is under significant stress. To this day, industry “leaders” still argue about what really caused the dislocation. Most recently, Star Xu, the CEO of OKX, indirectly pointed the finger at Binance’s marketing push around using USDe as collateral. Even though Sigil Stable keeps minimal exposure on centralized exchanges, we do not brush these accusations aside and adjust our exposure accordingly. Context matters, though: the Binance and OKX relationship has history, and the friction between CZ and Star Xu goes back years.

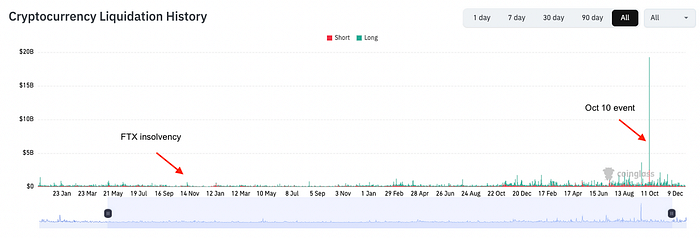

Let’s close this topic with one final look at the scale. Coinglass reported over $19b of liquidations on October 10, nearly 19x higher than the liquidation print around the FTX insolvency in early November 2022. The real number is likely higher still: the headline charts do not capture liquidations on several other large perpetual DEXs, on decentralized money markets, and CEX liquidation reporting can be incomplete (Binance broadcasts maximum one liquidation per second).

Oct 10 Liquidation History, source: Coinglass

As we reported in our previous quarterly letter, Sigil Stable closed the liquidation weekend without any loss.

Our risk management in practice

Roughly a month after October 10, DeFi served up the next course. Stream Finance attracted deposits by advertising around 18% APR. Under the hood, the system leaned on lending and borrowing its own assets, recycling borrowed tokens into partner vaults, and minting new yield tokens on top. The result was circular liquidity dressed up as organic growth, and TVL (total value locked) that went up and to the right until it didn’t.

Press enter or click to view image in full size

Stablecoin ouroboros. Source: AI-generated

The music stopped when Stream disclosed a $93m loss allegedly tied to external fund-manager exposure. Withdrawals were halted and xUSD depegged aggressively, trading as low as $0.10. The contagion spread into other “tokenized hedge fund” style products (e.g. Elixir Finance) and spilled into curated vaults managed by well-known risk managers across platforms such as Morpho and Euler. A full post-mortem deserves its own write-up, but our technical advisor Mikko has already gone deeper on the mechanics.

Sigil Stable had no exposure to Stream Finance, Elixir, or any of the affected curated vaults. In practice, neither protocol passed our initial smell test. Looking properly under the hood and assessing transparency is not optional when underwriting these systems, and we touched on that point in the Ethena section of our previous quarterly letter.

The DAT Discount

Following up on the Sigil Core section, digital asset treasury companies (DATs) had a sobering moment in Q4. The easiest way to see it is through mNAV (market cap relative to the NAV of crypto holdings) compressing across the board.

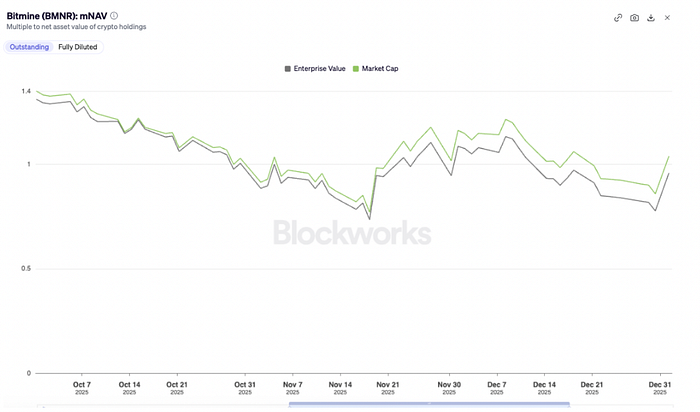

The mNAV of the flagship Ethereum DAT Bitmine compressed from 1.35 to 0.86, a 36% decline.

Bitmine mNAV. Source: Blockworks

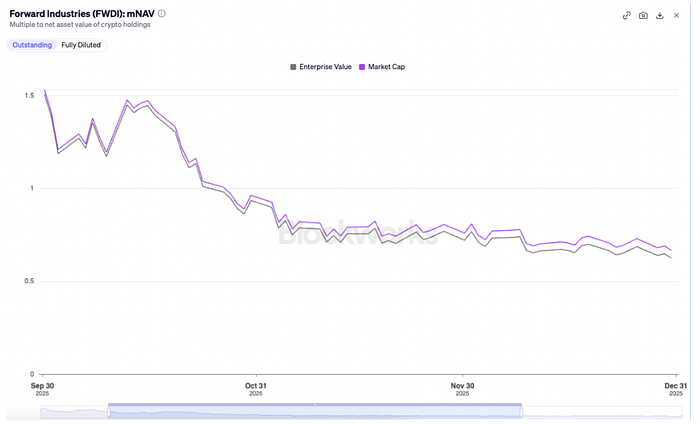

The move in the flagship Solana DAT Forward Industries was even more dramatic. Its mNAV declined by 56% and ended the year at 0.67. It’s worth remembering that Forward was trading at a sub-$20m valuation before raising $1.65b in a PIPE deal to buy SOL. The shares became effective one month later than anticipated in early November, roughly two months after the PIPE closed. By then, mNAV had already collapsed deep below 1.

Forward Industries mNAV source: Blockworks

Sigil Stable’s less-than-ideal performance in Q4 was primarily driven by our hedged exposure to Forward Industries as the company’s market cap closed the year more than 30% below its SOL reserves. The current position represents less than 1% of the portfolio and remains hedged. Forward is generating over 6% APR by staking its SOL. We expect part of the mNAV gap to close this year and reprice toward at least 0.85, which would support PnL even if SOL depreciates. At the same time, we agree with Mike Novogratz (Galaxy’s founder and one of Forward’s lead investors) that for DATs to trade sustainably above 1x mNAV again, management teams will need to turn these vehicles into real operating companies, with revenue streams beyond staking yield.

Portfolio Highlights — good news in the making

Following up on our Q3 letter, we remain extremely bullish on our private liquidity deal with USDai. USDai announced a $500m non-recourse guidance facility for QumulusAI (financing up to 70% of approved GPU deployments), then followed with a $200m guidance facility for Japan’s Quantum Solutions, making the “GPU mortgage” narrative increasingly concrete. And to round out the quarter, they landed Coinbase Ventures investment and announced a PayPal PYUSD integration plus a $1b customer incentive program.

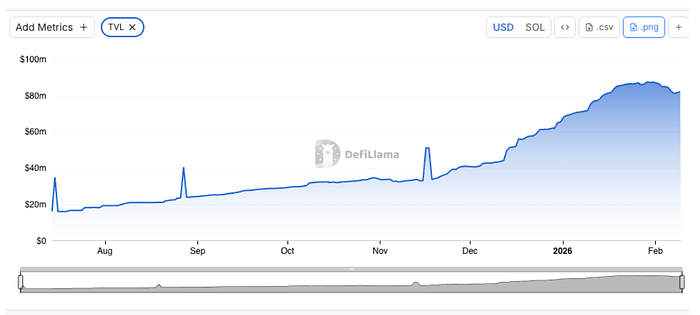

OnRe is essentially “reinsurance-on-chain”: a structure that lets capital earn an insurance-style return stream, but packaged in a crypto-native wrapper with transparent positioning and on-chain settlement. We closed a private liquidity deal with OnRe in December last year in both Sigil Stable and Sigil Core, because the setup looked like real underwriting economics rather than DeFi theater à la Stream Finance. Before wiring a dollar, we asked one of our Zurich-based investors, a Swiss Re veteran, to tear the product apart; his feedback was simple and encouraging: the structure was thoughtfully built, and the risk framing was unusually disciplined for crypto. In a market full of synthetic yield, OnRe is one of the few places where the yield is at least trying to be paid for by actual risk transfer.

The TVL has almost doubled since our allocation.

OnRe TVL source: DefiLlama

In conclusion

While Q4 performance was not ideal, we still finished the year at over +11% net profit after fees. More importantly, we navigated the unprecedented October 10 liquidation cascade and one of the largest DeFi contagions in recent years without any scars. We remain bullish on both our public and private allocations, including several positions where value is expected to be realized later as a one-time step function. Finally, we are continuing to expand our automated trading capabilities to improve speed and risk control while increasing the number of opportunities for our investors.

Thank you for your ongoing trust in Sigil Fund.

— Joe, Investment Partner heading Sigil Stable trading.

If you’d like to discuss your investment, please don’t hesitate to reach out to us at info@sigilfund.com.